CRE Asset Management

June 30, 2026

CRE Asset Management

June 30, 2026

According to Deloitte’s 2026 Banking and Capital Markets Outlook, data fragmentation and the inability to consolidate information across disconnected systems remain among the top operational constraints for financial institutions managing real estate credit exposure. For CRE investors and lenders, that fragmentation is the reason loan onboarding takes three weeks instead of three days, the reason rent roll data in one spreadsheet contradicts the T-12 in another, and the reason portfolio reviews require a week of manual reconciliation before a single decision can be made.

This analysis draws on Smart Capital Center, a CRE AI platform that has processed $500B+ in transactions across 120M+ properties, used by institutional investors, lenders, and asset managers including JLL and KeyBank to map the data management best practices for CRE that separate high-performing teams from those perpetually behind on reconciliation.

The scale of the problem is consistent across lender types. According to the Mortgage Bankers Association’s 2025 Commercial/Multifamily Finance Outlook, manual data re-entry and the absence of integrated data workflows remain among the most frequently cited operational inefficiencies by commercial lending teams, with lenders reporting that loan onboarding timelines are disproportionately extended by fragmented document handling rather than credit complexity. MBA Chief Economist Mike Fratantoni has noted publicly that “the operational infrastructure gap in commercial lending is a workflow integration problem, and lenders that close it first will have a structural efficiency advantage that compounds over time.”

The core data management in CRE problem is architectural. A typical lender or institutional investor touches six to ten distinct data types across every deal: rent rolls, T-12 operating statements, offering memorandums, appraisals, lease abstracts, loan origination documents, draw schedules, and loan servicing records. Each lives in a different format, produced by a different party, and stored in a different location.

This produces a version-control problem: multiple copies of the same document with different figures circulating across investment, relationship, and asset-management teams, with no authoritative source of record. Reconciling them manually is slow, error-prone, and, critically, does not scale when deal volume increases.

The failure modes are predictable. A rent roll with a manually entered occupancy figure that contradicts the T-12 revenue line gets averaged rather than investigated. A loan covenant threshold set at origination never gets connected to the loan servicing platform that would trigger an alert when it is approached. According to PwC’s Emerging Trends in Real Estate 2026, data infrastructure quality is now a top-three strategic differentiator for CRE firms, and the gap between firms with unified data layers and those still reconciling across spreadsheets is widening with each deal cycle.

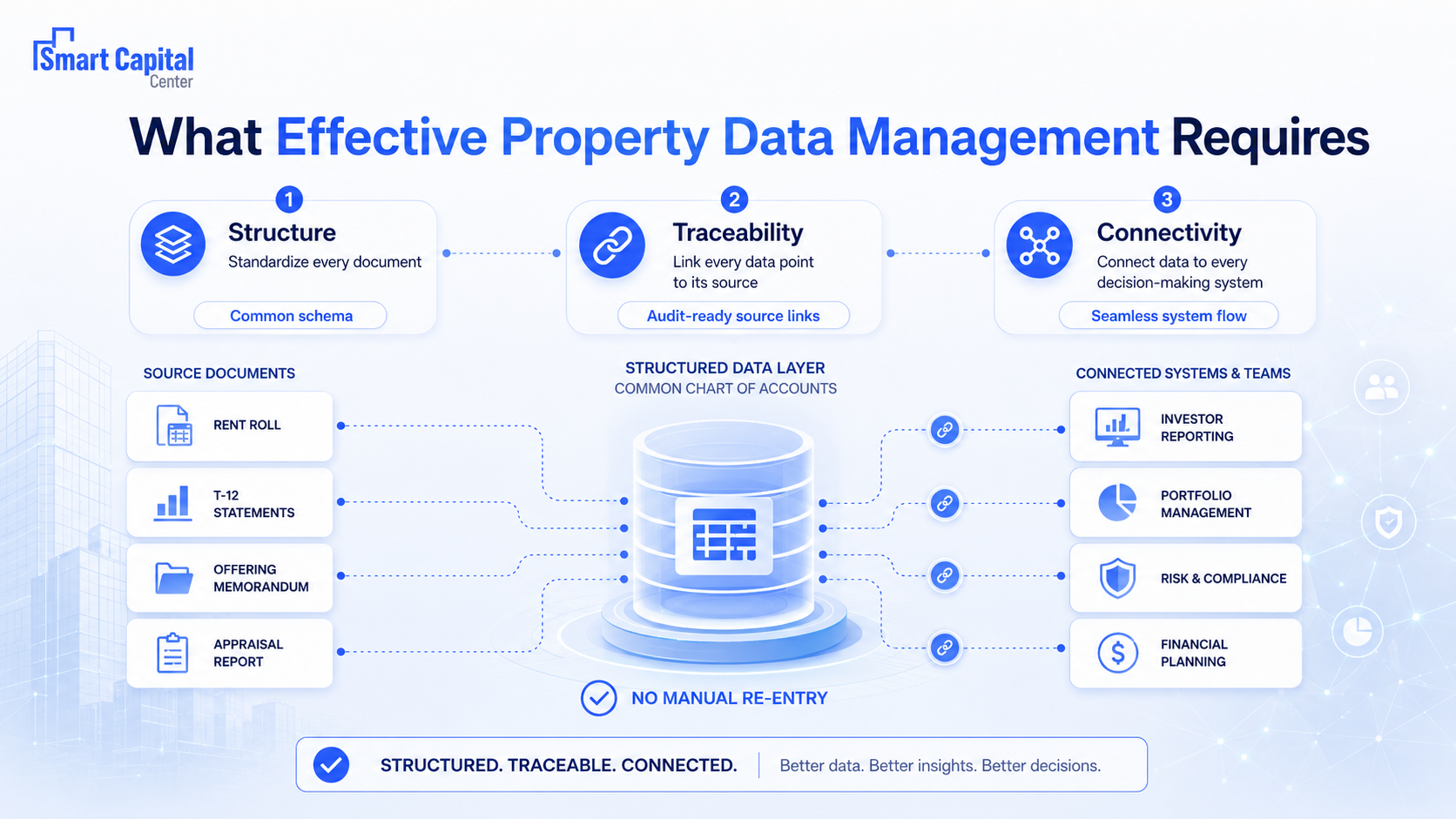

Effective property data management depends on three things: structure, traceability, and connectivity: whether the data extracted from a source document is standardized consistently, linked to its origin, and accessible to every team that needs it without a manual bridge.

Three requirements define whether a data management approach works in practice:

• Standardization: Every financial document uses different line-item labels, expense categories, and formatting conventions. “Base rent” in one OM is “Gross rental income” in another. Without a common chart of accounts applied consistently at ingestion, cross-asset benchmarking is impossible and portfolio aggregation produces apples-to-oranges comparisons.

• Source traceability: Every data point should be linkable back to the document from which it was extracted. If a DSCR figure in a credit package cannot be traced to the specific T-12 line that generated it, the audit trail is broken before it reaches the credit committee.

• System connectivity: Data extracted from documents must flow into the platforms where decisions are made without a manual re-entry step. Every handoff between systems is a reconciliation risk and a lag point.

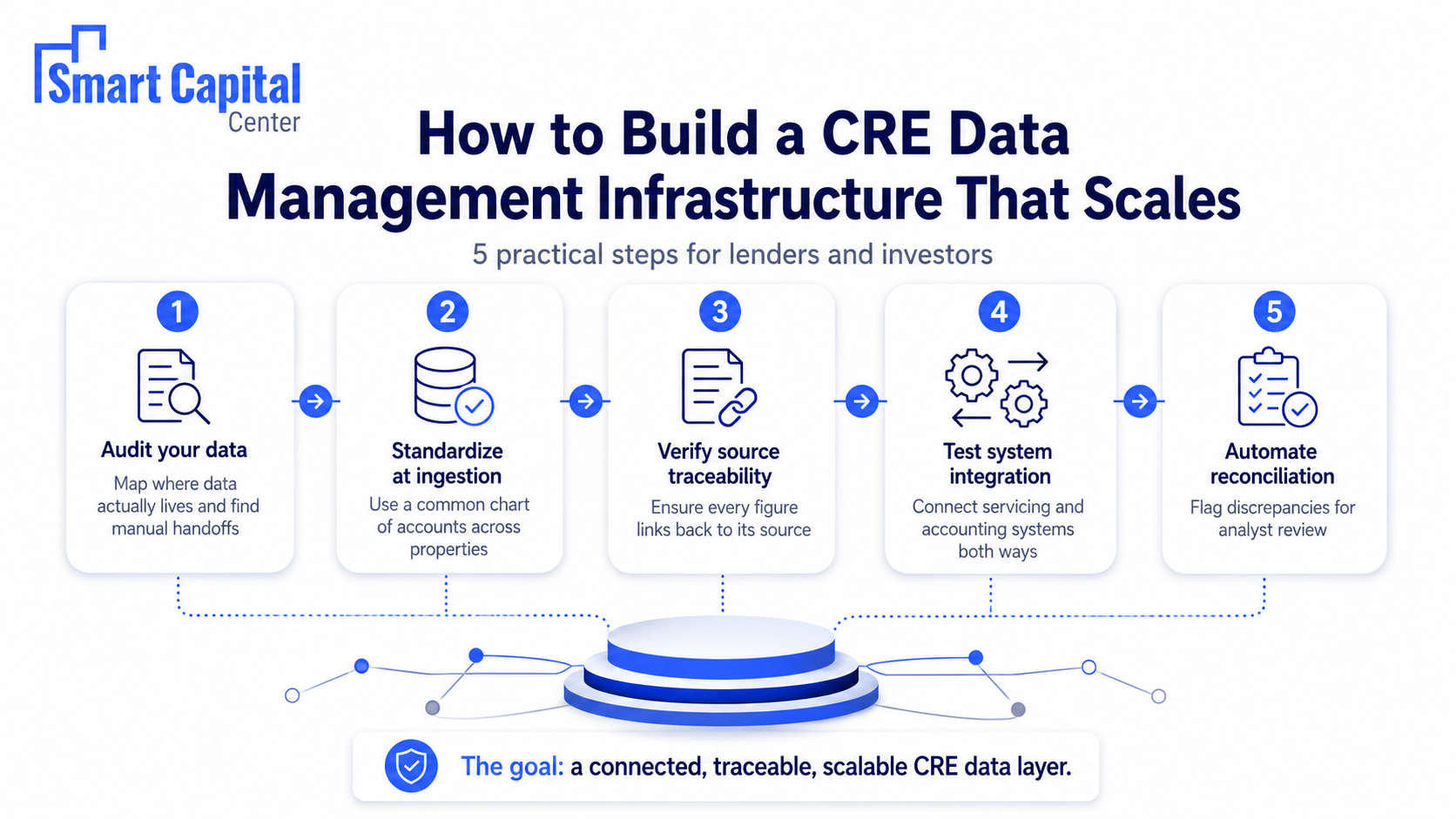

The ingestion stage is where most data management in real estate problems originate and where the highest-leverage fixes apply. Getting this stage right means that everything downstream starts from clean, consistent data.

The most durable fix is a common chart of accounts applied at ingestion: a standardized schema that maps incoming line items from any document or operator format into a consistent set of categories. Once established, this structure reuses across every future upload, and accuracy improves as the dataset grows. Smart Capital Center’s AI layer applies this standardization automatically, mapping T-12 and operating statement line items to a consistent schema regardless of how the originating property manager labeled them.

What this means in practice: the chart of accounts is also the benchmarking infrastructure. Teams that standardize at ingestion are building the database that makes cross-asset expense ratio comparisons, NOI benchmarking, and portfolio aggregation possible. Teams that skip this step spend that time on reconciliation instead.

The practical barrier to consistent ingestion has historically been document quality: scanned PDFs, handwritten annotations, broker-formatted OMs with no standard layout, and appraisals with key figures buried 40 pages in. AI-powered extraction removes this barrier.

Smart Capital Center ingests rent rolls, T-12s, OMs, appraisals, lease abstracts, and even handwritten notes in any format. Every figure extracted is linked to its source document, clickable for review, and flagged when confidence is below the threshold for auto-approval. The result is structured, audit-ready data from documents that previously required hours of manual processing. JLL documented a 30x productivity gain in financial statement processing after deploying this layer, reducing per-document time from 30–40 minutes to under 3 minutes.

Data governance is the infrastructure that makes data management defensible in front of credit committees, LP auditors, and bank examiners. Three elements define whether a governance framework functions:

KeyBank reported a 40% reduction in loan model preparation time after deploying Smart Capital Center’s data infrastructure layer, with the gains attributable to eliminating manual reconciliation steps between document-based data and model inputs, not just extraction speed alone.

The operational cost of fragmented data infrastructure extends beyond loan onboarding speed. According to the MBA’s 2024 Annual Convention & Expo research briefing, commercial lenders operating without integrated data layers spend an estimated 20–35% of origination team capacity on manual data reconciliation tasks that generate no credit output, a figure that scales linearly with portfolio growth unless the underlying data architecture is addressed. For lenders evaluating where to close this gap first, the origination-to-servicing data handoff is consistently identified as the highest-cost reconciliation point in the workflow.

A static data warehouse captures what was true when the document was processed. A real-time intelligence layer reflects what is true now. For most CRE decisions, the difference between those two is measured in weeks, and weeks matter.

Smart Capital Center’s platform combines document-level data extraction with 1B+ real-time market signals across 120M+ properties, giving lenders and investors a live view of both their portfolio’s financial position and the market conditions surrounding it. Covenant metrics update as new documents are ingested. Collateral valuations reflect current cap rate movements, not the appraisal from 18 months ago.

The failure modes in CRE data management are consistent across firm types and deal sizes. Three carry the most financial weight:

A DSCR threshold embedded in a loan agreement triggers a lender’s response obligation when breached. If the financial data driving the DSCR calculation updates in the accounting platform but never flows to the covenant monitoring layer, the breach can persist for an entire reporting cycle before anyone sees it. It is the standard outcome when servicing, accounting, and loan management systems do not share a data layer.

Smart Capital Center mitigates this through native integration with Yardi, SS&C Precision, Midland Enterprise, and ARGUS, connecting document-extracted financial data directly to covenant monitoring workflows with automated alerts the moment a threshold is approached, not at the next reporting cycle.

A credit committee reviewing a loan package that contains a rent roll from one date and a T-12 from another with no clear indication which is current is making a decision on a document set that may not reflect the same moment in time. This version-control gap is common across teams managing data across email threads and shared drives, and it produces exactly the kind of inconsistency that audit functions and bank examiners flag during credit reviews.

Smart Capital Center mitigates this through a document history layer that timestamps every ingested file, flags when newer versions of a document are available, and maintains a clear record of which version of each input populated any given output, so a credit package always reflects a consistent, dated dataset.

Automated extraction accelerates ingestion, but treating AI output as ground truth without a reconciliation step introduces a new failure mode: confidently wrong data that passes through unreviewed. This is particularly consequential for contingent lease provisions, expense adjustments buried in footnotes, or handwritten amendments that modify printed terms.

Smart Capital Center mitigates this through exception management that flags low-confidence extractions and inconsistencies between document-based figures for analyst review, rather than routing them directly into models. Every extracted figure is linkable to its source for spot-check review.

Smart Capital Center satisfies all five steps, including native integrations with the platforms institutional lenders and investors already use, and a reconciliation layer designed to surface conflicts rather than paper over them. For a deeper look at how unified data intelligence works across CRE deal types, see Commercial Real Estate Data: The Unified Intelligence Guide.

The teams closing more deals, catching risk earlier, and scaling without proportional headcount increases are not doing so because their data is structured, current, and connected to the workflows where decisions are made.

Smart Capital Center's data infrastructure combines AI-powered extraction from any document format, a common chart of accounts applied at ingestion, full source-level traceability, automated reconciliation, and real-time market intelligence across 120M+ properties, all integrated with the loan servicing, accounting, and asset management platforms institutional lenders and investors already operate.

Stop reconciling across spreadsheets and start managing from a single, current data layer. Book a demo with Smart Capital Center today.

The highest-leverage practices are standardizing financial data to a common chart of accounts at ingestion, maintaining full source-level traceability on every extracted figure, and integrating document-based data with loan servicing and accounting platforms without a manual re-entry step. The practice most consistently missed is automated inconsistency detection, building a reconciliation layer that surfaces conflicts between document-based data and system data for human review, rather than allowing them to persist undetected across reporting cycles.

AI-powered extraction processes unstructured documents in minutes rather than hours, applies consistent extraction criteria across every document, and flags low-confidence results for analyst review rather than passing them through silently. The more durable advantage is structural: every figure AI extracts is linked to its source document, creating the audit trail that manual extraction rarely produces. JLL documented a 30x productivity gain in financial statement processing after deploying Smart Capital Center’s extraction layer, with per-document time dropping from 30–40 minutes to under 3 minutes.

Leading AI extraction platforms handle the full range of CRE document types: rent rolls, trailing twelve-month operating statements, offering memorandums, appraisals, lease agreements, draw requests, and loan origination documents. Smart Capital Center processes all of these in any format, without requiring a clean export or standardized template from the submitting party. Extracted data is mapped to a consistent schema and linked to its source for review.

Look for platforms with native integrations rather than generic API connections that require custom development. Smart Capital Center integrates directly with Yardi, SS&C Precision, Midland Enterprise, and ARGUS, meaning extracted data flows into existing workflows without re-entry. Before committing to any data management platform, test the integration with your actual systems: confirm that data moves in both directions, that the connection does not require a manual export step, and that the CRE software handles your specific document types and asset classes without customization.

Real-time market intelligence is what separates a data warehouse from an operational decision-making layer. Document-extracted data captures the financial position of a property at a specific point in time. Real-time market signals provide the market context needed to evaluate whether that financial position is strengthening or deteriorating relative to current conditions. Smart Capital Center combines both in a single platform, giving lenders and investors a live view of portfolio performance and market conditions simultaneously.