AI in Commercial Real Estate

June 16, 2026

AI in Commercial Real Estate

June 16, 2026

A single CRE acquisition can generate 800 to 1,200 pages of legal, financial, and operational documentation — loan agreements, rent rolls, T-12 financial statements, lease abstracts, insurance certificates, title reports, and property records. According to Deloitte's 2026 Commercial Real Estate Outlook, document preparation and review now consume a disproportionate share of analyst time at the moments where speed matters most — origination, credit approval, and quarterly reporting. For CRE lenders and investors still reviewing those documents by hand, the bottleneck is not just operationally inefficient. It directly determines how many deals a team can pursue, how quickly they can commit, and how many opportunities they lose to better-prepared competitors.

This analysis draws on Smart Capital Center — a CRE AI platform validated across $500B+ in transactions and 120M+ properties, trusted by institutional lenders, investors, and asset managers including JLL and KeyBank — to map exactly how AI document analysis works across the loan, lease, insurance, and property record workflows that drive CRE decisions today.

AI document analysis in commercial real estate refers to the automated extraction, structuring, and interpretation of data from CRE-specific documents — loan agreements, rent rolls, T-12 financial statements, lease abstracts, insurance certificates, title reports, and property records — using natural language processing and domain-trained models that understand the structure, terminology, and clause conventions of institutional real estate finance.

Unlike generic OCR or basic text-extraction tools, AI document analysis built for CRE applies semantic, clause-level analysis. It recognizes that a co-tenancy clause is operationally different from a subletting clause, that a lender's loss payable endorsement on an insurance certificate carries specific compliance significance, and that a kick-out clause buried in a lease exhibit is materially different from a base termination right. The model is calibrated to the document patterns institutional CRE actually produces — not generalized from contracts across industries.

For institutional users, three capabilities define a CRE-specific document analysis platform: clause-level semantic understanding rather than keyword matching, full source-level traceability from extracted figure back to original document line, and integration directly into the underwriting, asset management, and reporting workflows where the data is actually applied.

Manual document review in commercial real estate carries three structural problems that compound as portfolio size and deal velocity increase.

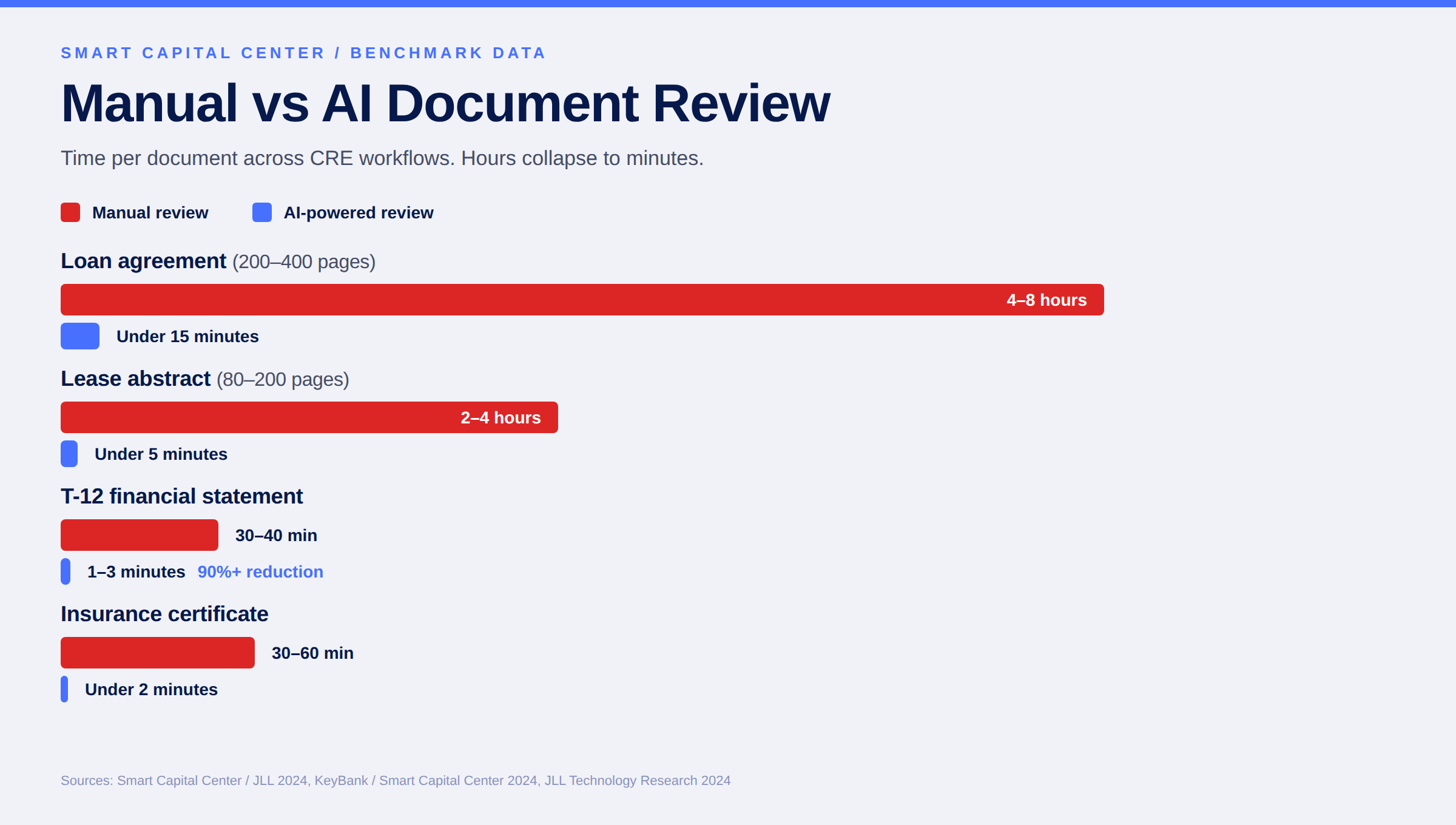

Time. A thorough manual review of a 300-page loan agreement takes 4 to 8 hours. A standard commercial lease takes 2 to 4 hours per document. A T-12 financial statement takes 30 to 40 minutes. For a regional bank originating ten loans per month, that's 120+ analyst hours per cycle on initial document review alone — before any portfolio monitoring, renewal review, or compliance check.

Error rate. Different analysts abstract differently. Provisions one reviewer flags as material another may summarize briefly or omit. Manual extraction error rates in document-intensive financial workflows run materially higher than automated extraction with source-level validation — and the errors are not random. They concentrate in exactly the clause categories that carry the highest financial consequence: covenants, special conditions, contingent provisions, and exception clauses.

Scalability ceiling. Manual review scales linearly with headcount. A team that processes 50 documents per month at acceptable quality cannot process 200 without proportional staffing. For growing portfolios, this creates a binary choice: accept slower processing or hire continuously to keep up. Neither option preserves margin in a competitive market.

According to KPMG's research on generative AI in real estate, document review and data extraction rank among the highest-ROI applications of AI in the asset class — precisely because the manual baseline is so costly. The efficiency gains compound rapidly as portfolio size increases.

The performance gap between manual and AI-powered document review is documented across institutional sources. The table below aggregates named benchmarks by document type to show where AI delivers the most measurable impact.

The 70% figure from the MBA Finance Servicing and Technology Conference comes from a live poll of conference attendees — institutional lenders and servicers — who estimated how much of their current document review work could be automated with current AI capabilities. That estimate is consistent with PwC's Emerging Trends in Real Estate 2026, which identifies AI and data analytics adoption as a top-three strategic priority for CRE firms entering the next market cycle.

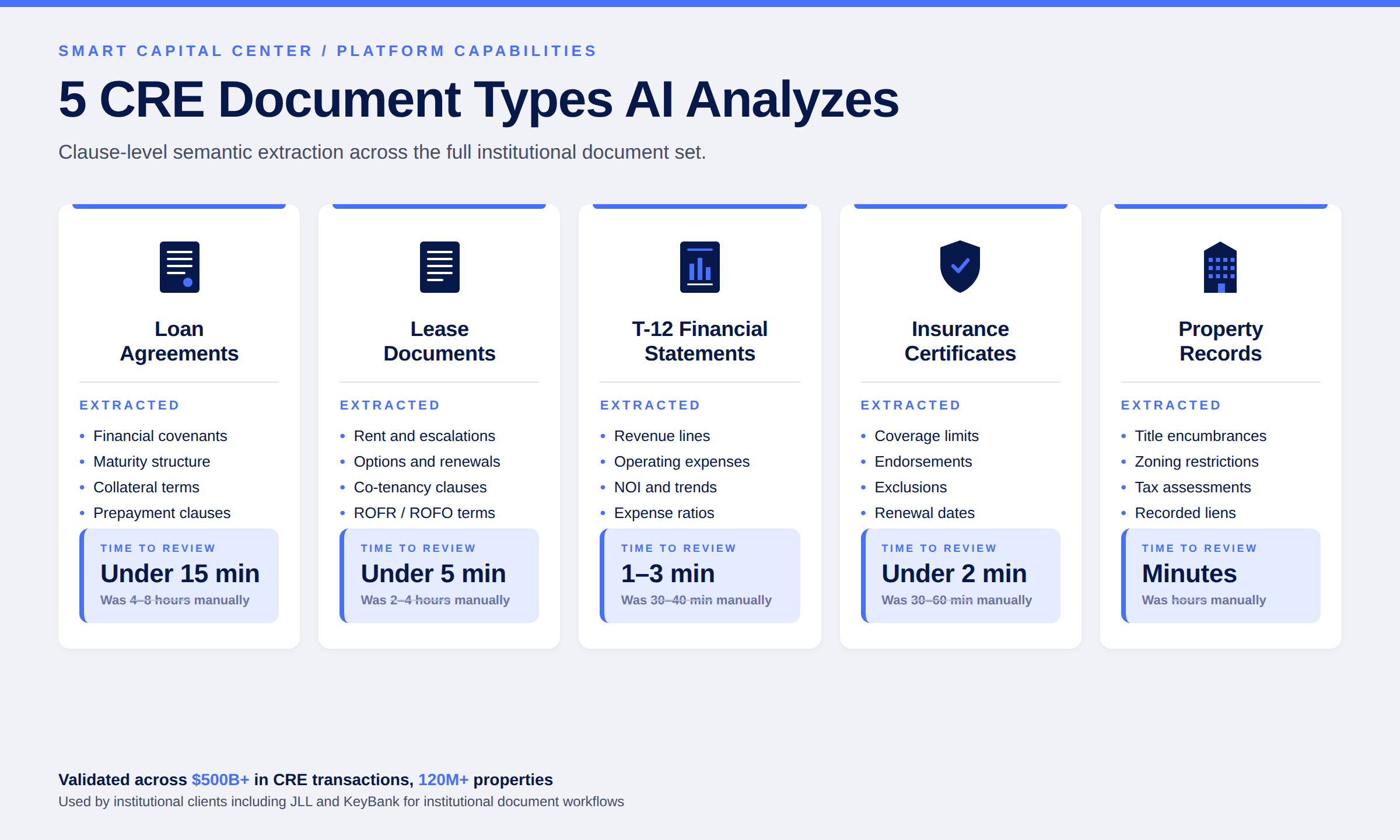

Smart Capital Center's loan document module ingests the full agreement — typically 200 to 400 pages for a standard institutional CRE loan — and applies clause-level extraction across the financial covenants (DSCR, debt yield, LTV minimums), maturity structure (initial term, extension options, prepayment provisions), collateral terms (primary collateral, additional security, cross-collateralization), and notice and reporting requirements. Each extracted item links back to the exact clause in the source document, creating a complete audit trail for credit and compliance functions. What previously consumed 4–8 hours of analyst review is completed in under 15 minutes.

Insurance compliance is one of the highest-volume, lowest-margin workflows in CRE servicing. A portfolio of 200 loans generates 200+ insurance certificates per year — each requiring verification of coverage limits, exclusions, named insured matching, deductible alignment with loan terms, and the specific endorsements lenders require (mortgagee clauses, lender loss payable, additional insured language). Smart Capital Center's insurance module extracts and validates every component automatically, flagging missing endorsements, expired policies, and coverage gaps before they create regulatory or recovery exposure. What previously took 30–60 minutes per certificate is reduced to under 2 minutes — with consistent criteria applied across every certificate in the portfolio.

Lease abstraction is the document workflow most prone to error in manual review — both because commercial leases run 80 to 200 pages and because the provisions that matter most (co-tenancy clauses, contingent rent abatements, kick-out rights, ROFO/ROFR provisions, expansion options) are often buried in exhibits and addenda. Smart Capital Center's lease abstraction module applies semantic clause-level analysis trained across millions of CRE lease documents — meaning a rent abatement tied to a landlord delivery condition is correctly classified as a contingent financial term, not a static concession. Every extracted provision links back to its source clause.

Title reports, zoning records, tax records, and environmental disclosures each carry deal-breaking risk if reviewed incompletely. Smart Capital Center's property record module extracts and structures the operative items from each document type — title encumbrances, easements, zoning restrictions, current and historical tax assessments, recorded liens, and any flagged environmental conditions — and presents them in a deal-ready summary that surfaces issues during initial review rather than mid-diligence.

At the MBA Finance Servicing and Technology Conference, where Smart Capital Center was showcased to institutional lenders and servicers, attendees estimated that up to 70% of current document review work could be automated. Laura Krashakova, CEO of Smart Capital Center, addressed the operational implications directly:

"If asset management and servicing teams can shift hours from manual document review to analyzing portfolio risk, we can prevent losses, accelerate decisions, and meaningfully improve outcomes. The platforms that get this right are not just speeding up document review — they are turning documents from a bottleneck into a continuous source of portfolio intelligence."

For lenders and asset managers deploying AI document analysis across active loan books, three specific risks carry material financial and compliance weight. Each warrants an explicit mitigation strategy.

An automated insurance review system that processes the most recent certificate on file — without verifying whether a renewal has been issued, lapsed, or modified — can generate a compliance signal that reflects last year's coverage rather than current conditions. A servicer relying on stale extraction may miss a coverage gap on a property whose policy quietly expired, or pass a certificate that no longer matches the loan's required endorsement structure.

SCC mitigates this through continuous certificate ingestion that tracks renewal dates per policy and flags any certificate within 30 days of expiration. Each extraction is timestamped, and certificates approaching renewal trigger automated alerts to the servicing team before coverage gaps occur.

Executed CRE documents — loan agreements, lease amendments, insurance endorsements — frequently contain handwritten amendments, initialed modifications, and margin annotations that alter the printed terms in legally binding ways. A basic OCR or text-extraction layer that reads the printed page but ignores handwritten content can produce a materially incomplete abstract — missing a rent reduction agreed at signing, a modified notice period, or a superseded covenant threshold.

Smart Capital Center mitigates this through multi-model parsing that combines OCR, layout analysis, and handwriting recognition to process both printed and handwritten content. Low-confidence extractions — including those affected by annotation legibility or atypical placement — are automatically flagged for analyst review rather than passed through silently.

A document analysis model trained on a broad corpus of business contracts will not reliably distinguish between a CRE-specific co-tenancy clause and a generic exclusivity provision, or between a lender loss payable endorsement and a standard mortgagee clause. Generic AI categorization in a CRE context produces output that is structurally complete but semantically wrong — and the errors concentrate in exactly the clauses that carry the highest financial consequence.

SCC mitigates this through proprietary language models trained specifically on institutional CRE documents — millions of loan agreements, leases, insurance certificates, and property records across every major asset class. The model recognizes CRE clause patterns natively, not by adaptation from a general-purpose extractor.

These five criteria separate genuinely useful CRE document analysis platforms from generic document tools dressed up with AI marketing language.

Step 1: Test extraction on your own documents, not the vendor's sample. Upload a complex loan agreement, a multi-tenant lease with exhibits, and an insurance certificate from your active portfolio. Confirm the platform correctly extracts covenants, contingent provisions, and required endorsements — not just base rent, maturity date, and coverage amount. A vendor demo using a preloaded sample file is not a meaningful test.

Step 2: Verify source-level traceability on every extracted figure. Every figure in the extracted output should be clickable back to its exact line in the source document. Request a sample extraction and trace one figure — a DSCR covenant threshold, a co-tenancy trigger, a coverage limit — back to the originating clause. If the platform cannot demonstrate this, it cannot meet the audit standard institutional compliance functions require.

Step 3: Confirm CRE-specific model training, not general adaptation. Ask the vendor explicitly: was the language model built for CRE, or adapted from a general-purpose extractor? Platforms trained on millions of CRE-specific documents handle clause-level nuance materially differently than those adapted from generic contract analysis tools.

Step 4: Audit handwriting and annotation handling. Test the platform on a scanned document with handwritten amendments or margin annotations. If the platform cannot identify and extract handwritten content — or flag low-confidence extractions for analyst review — modified terms will pass through undetected.

Step 5: Validate integration with underwriting and servicing workflows. Document extraction is only useful if the structured output flows directly into the systems where analysts work. Confirm the platform integrates with Yardi, SS&C Precision, and the underwriting models your team already uses — without manual export or reformatting steps.

Smart Capital Center passes all five tests — built by veteran CRE professionals, trained on $500B+ in transactions, with multi-model parsing for handwritten content, full source-level traceability, and direct integration into institutional underwriting and servicing workflows.

AI document analysis does not change what CRE lenders, investors, and asset managers need from a loan agreement, a lease, or an insurance certificate — it changes how quickly and consistently that information can be extracted, validated, and acted on. The teams that automate document review today are not just reclaiming analyst hours. They are building the institutional data infrastructure that separates defensible underwriting from exposure they cannot see.

Smart Capital Center brings together CRE-specific language models, multi-model document parsing, source-level traceability, and direct integration into the underwriting and servicing workflows where extracted data actually applies. The result: complete, audit-ready document analysis in minutes, not hours — across loan agreements, leases, insurance certificates, and property records simultaneously.

Cut document review from days to minutes across every document type your team handles. Book a demo with Smart Capital Center today.

What types of CRE documents can AI analyze?

AI document analysis platforms built for commercial real estate handle the full range of institutional document types: loan agreements, rent rolls, T-12 financial statements, leases and lease amendments, insurance certificates, title reports, zoning and tax records, property condition assessments, and environmental disclosures. Smart Capital Center's AI module is calibrated to each document type — meaning a loan agreement is parsed for covenants, maturity, and collateral, while an insurance certificate is parsed for coverage limits, endorsements, and policy currency. The clause-level depth is what separates CRE-specific platforms from generic document extractors.

How much time can my team realistically save on document review with AI?

The benchmark data is consistent across institutional sources: financial statement processing drops from 30–40 minutes per document to 1–3 minutes (90%+ reduction, per JLL deployment data); lease abstraction drops from 2–4 hours per document to under 5 minutes; loan agreement review drops from 4–8 hours per document to under 15 minutes; and full credit memo generation drops from 4–8 hours per deal to under 30 minutes. For a regional bank originating ten loans per month, this represents 100+ analyst hours reclaimed monthly — capacity redirected to underwriting judgment, portfolio risk analysis, and borrower relationships.

Can AI handle complex CRE documents like 300-page loan agreements?

Yes — and the time advantage compounds with document length. A 300-page institutional CRE loan agreement that requires 4–8 hours of careful manual review is processed by Smart Capital Center's loan document module in under 15 minutes, with covenants, maturity structure, collateral terms, and reporting requirements all extracted with source-level traceability. The clause-level depth is consistent regardless of document length, because the model reads every page at the same standard rather than triaging by reviewer fatigue.

How does AI document analysis fit into my existing CRE workflows?

Document extraction is most valuable when the structured output flows directly into the systems where analysts already work. Smart Capital Center integrates natively with Yardi, SS&C Precision, and other property management and accounting platforms — meaning extracted data populates underwriting models, portfolio dashboards, and credit packages automatically, without manual re-entry or reformatting. The platform also generates structured outputs for compliance audit trails, eliminating the documentation burden that periodic manual review cannot demonstrate to examiners.

Can I trust AI-extracted data in a credit package or investment committee submission?

Institutional-grade AI document analysis meets compliance accuracy standards when the platform is trained specifically on CRE documents, provides full source-level traceability on every extracted figure, and applies exception management for low-confidence extractions. Smart Capital Center has been validated across $500B+ in CRE transactions and is used by institutional firms including JLL and KeyBank for document analysis directly in credit and asset management workflows. JLL reports a 90%+ reduction in document processing errors after deployment. For loan committee or investment committee submissions, every figure in a generated package is clickable back to its source document — making analyst validation faster, not optional.