AI in Commercial Real Estate

July 30, 2026

AI in Commercial Real Estate

July 30, 2026

According to KPMG’s 2025 Generative AI in Real Estate Report, hallucination rates in general-purpose AI tools applied to structured financial documents remain a primary adoption barrier for CRE lenders and investors, with the majority of institutional respondents citing output verifiability as their top requirement before deploying AI commercial real estate underwriting tools in live deal workflows. That concern is rational. A generic AI tool that confidently extracts a wrong figure from a rent roll and populates it into a DSCR model is dangerous in a way that a manual error is not, because it carries the appearance of systematic validation.

This analysis draws on Smart Capital Center, a CRE AI platform that has processed $500B+ in transactions across 120M+ properties, used by institutional lenders and investors including KeyBank and JLL, to map what trustworthy CRE underwriting AI requires and how to evaluate any platform against those standards before adopting it.

The regulatory stakes for AI model accuracy in financial services have been formally articulated by the agencies that oversee the industry. In OCC Bulletin 2026-13, the OCC, Federal Reserve, and FDIC issued updated interagency Model Risk Management guidance that explicitly states: “Use of models also can present substantial risk. Such risk, generally referred to as ‘model risk’ for purposes of this guidance, can lead to financial loss, errors in financial statements and reporting, and flawed financial and risk management decisions.” The same bulletin notes that the agencies plan to issue a request for information on banks’ use of AI specifically, including generative AI and agentic AI. For CRE lenders and investors deploying AI underwriting tools, this regulatory posture means that model accuracy, auditability, and human oversight are the framework under which these tools will be examined.

The skepticism CRE professionals bring to AI tools for underwriting commercial real estate deals is the appropriate response to a well-documented set of failure modes that generic AI tools exhibit when applied to financial documents:

• Hallucination: Large language models generate plausible-sounding content that is factually incorrect. In a rent roll context, this means confidently extracting a base rent figure that was never in the document, or conflating two tenants’ line items into one.

• Mistake confidence for correctness: Generic AI tools rarely surface their own uncertainty. A figure extracted with 60% confidence looks identical in the output to one extracted with 99% confidence, leaving the reviewer no signal about where to focus verification effort.

• Not understanding the context: A general-purpose model does not understand that a footnote modifying a base rent clause in a CRE lease changes the headline figure on the page above it. Domain-trained models handle these document structures. Generic models do not.

• No audit trail: If the AI cannot show you where a figure came from, there is no basis for verification. The output cannot be trusted because it cannot be checked.

Each of these is a legitimate reason to withhold trust. The right question is whether a specific platform has addressed each of these failure modes with verifiable architecture.

According to McKinsey’s 2025 State of AI Survey, authored by Alex Singla, Alexander Sukharevsky, Lareina Yee, and Michael Chui of McKinsey’s QuantumBlack practice, organizations deploying domain-specific AI tools (models trained on the document types, vocabulary, and logical structures of a particular industry) report error rates 40–60% lower than those using general-purpose models adapted to the same task. “Full scaling will require redesigning workflows around AI capabilities,” the authors note, “and establishing the operating discipline to make those workflows reliable.” In CRE underwriting, that discipline means source traceability, automated reconciliation, and confidence signaling.

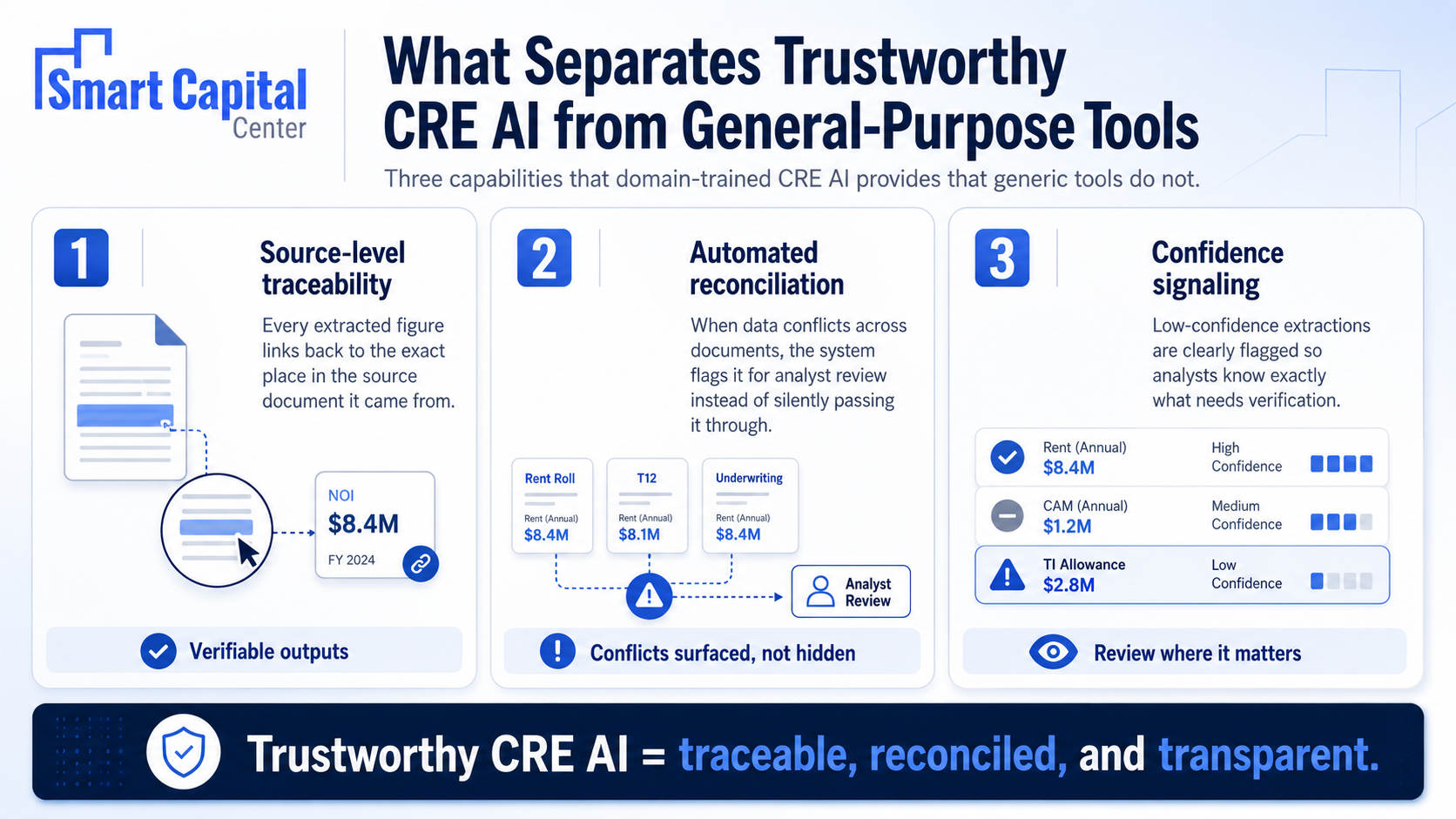

The practical difference is visible in three capabilities that generic tools do not have and domain-trained CRE AI does:

1. Source-level traceability: Every figure the AI extracts is linked to the exact location in the source document from which it came. A DSCR in a credit memo is one click away from the T-12 line that generated the NOI input. A base rent figure is one click from the lease clause. If a platform cannot demonstrate this, its outputs cannot be verified.

2. Automated reconciliation: When extracted data from one document conflicts with data from another – a rent roll occupancy rate that contradicts the T-12 revenue line, a lease term that does not match the OM summary – a trustworthy platform flags the discrepancy for analyst review rather than silently resolving it or passing it through. Smart Capital Center surfaces reconciliation issues for human attention. It does not auto-approve conflicting data.

3. Confidence signaling: The system communicates its own uncertainty. Low-confidence extractions are flagged differently from high-confidence ones, directing analyst review to precisely the outputs that warrant it. A reviewer who knows the system is uncertain about a particular figure can verify it. A reviewer who has no uncertainty signal must verify everything, which eliminates the efficiency benefit.

The most common misframing of AI in commercial underwriting is that the goal is full automation. The right framing is the opposite. AI handles mechanical work that does not require judgment: document ingestion, data extraction, model population, and initial memo drafting. The analyst handles what does require judgment: verifying inputs that matter, adjusting assumptions to market conditions, and making the credit decision.

According to the CREFC 2025 Lender Sentiment Survey, human override capability and analyst control rank as the top two institutional adoption requirements for AI commercial loan underwriting tools, above speed and cost savings. Smart Capital Center reflects this directly: every output is framed as an analyst-reviewed draft, every figure is verifiable, and every assumption is overridable.

Not all AI underwriting risks are equal. Three specific failure modes carry the most financial and compliance weight for lenders and investors:

A misread occupancy rate or transposed rent figure that populates a DSCR model without triggering a review flag produces a confident-looking output built on a wrong input. The error is not caught because nothing in the workflow signaled that it existed.

Smart Capital Center mitigates this through source-level traceability on every extracted figure and automated reconciliation that flags discrepancies between documents before they reach the model, rather than surfacing them after a committee questions the numbers.

When a platform presents all outputs uniformly regardless of extraction certainty, the analyst has no signal about where to concentrate verification effort. Everything looks equally reliable. Nothing is.

Smart Capital Center mitigates this through explicit confidence signaling: low-confidence extractions are flagged differently and routed for analyst review, so scrutiny concentrates on the outputs that warrant it rather than requiring uniform re-verification of every figure.

Write-ups that summarize market conditions, tenant profiles, or risk factors using AI-generated language without citations create the hallucination problem in its most consequential form: a committee reads a narrative that sounds authoritative but has no verifiable basis.

Smart Capital Center mitigates this through source-backed AI write-ups where every claim in a generated narrative is linked to the underlying data or document that supports it, giving reviewers the ability to verify the narrative as easily as the numbers.

The CRE professionals who have successfully adopted AI in their underwriting workflows are those who evaluated specific platforms against specific verifiability standards, and found systems whose architecture earns trust through traceability, reconciliation, and analyst control rather than asking for it through marketing claims.

Smart Capital Center’s AI tools for underwriting commercial real estate deals are built around this principle: every figure linked to its source, every discrepancy surfaced for review, every output framed as a draft the analyst controls. The question is whether the platform gives you the tools to verify it.

See exactly how Smart Capital Center handles extraction confidence, reconciliation flags, and source traceability on your own documents. Book a demo today.

The only reliable test is source traceability. If every figure an AI tool extracts is clickable back to the exact location in the source document that generated it, you can verify any output instantly. If the tool produces figures without source links, you have no mechanism to distinguish accurate extractions from hallucinated ones, and the only protection is manual re-verification of every figure, which eliminates the efficiency benefit. Before adopting any AI underwriting platform, run the source-link test on a live document from your own portfolio.

Domain-specific training and verifiable architecture. Generic AI tools are trained for general language tasks, not for the structural conventions of CRE financial documents, where a footnote can override a headline figure, where lease provisions interact with rent roll summaries, and where accounting conventions vary by operator. According to McKinsey’s 2025 AI Survey, domain-specific models report error rates 40–60% lower than general-purpose tools on the same financial document tasks. Beyond training, the architecture matters: source traceability, confidence signaling, and automated reconciliation are features that generic tools do not have.

It should flag it explicitly and route it for analyst review, not pass it through with the same presentation as a high-confidence extraction. A trustworthy CRE AI platform differentiates between figures it extracted with high certainty and those where document quality, ambiguous formatting, or conflicting data reduced extraction confidence. Smart Capital Center surfaces low-confidence extractions separately, so the analyst’s review effort concentrates on the outputs that warrant scrutiny rather than requiring uniform re-verification of every figure.

Yes, when the platform is designed around analyst review rather than autonomous output. Smart Capital Center frames all AI-generated outputs as analyst-reviewed drafts: every figure is verifiable before the package advances, every assumption is overridable, and every narrative section is reviewer-controlled. The credit package that goes to committee reflects analyst judgment applied to AI-assisted analysis. That distinction is the difference between a tool that earns institutional trust and one that creates liability.

Run five specific tests before adoption: ask for a source link on any figure in a live demo; submit a document with a deliberate internal inconsistency and verify the platform flags it; request a low-confidence extraction scenario and confirm the system surfaces it differently; verify analyst override at every output stage; and pull a compliance audit trail from a completed analysis to confirm it meets regulatory documentation standards. These tests separate platforms whose trust architecture is genuine from those where verifiability remains a marketing claim.