AI in Commercial Real Estate

July 9, 2026

AI in Commercial Real Estate

July 9, 2026

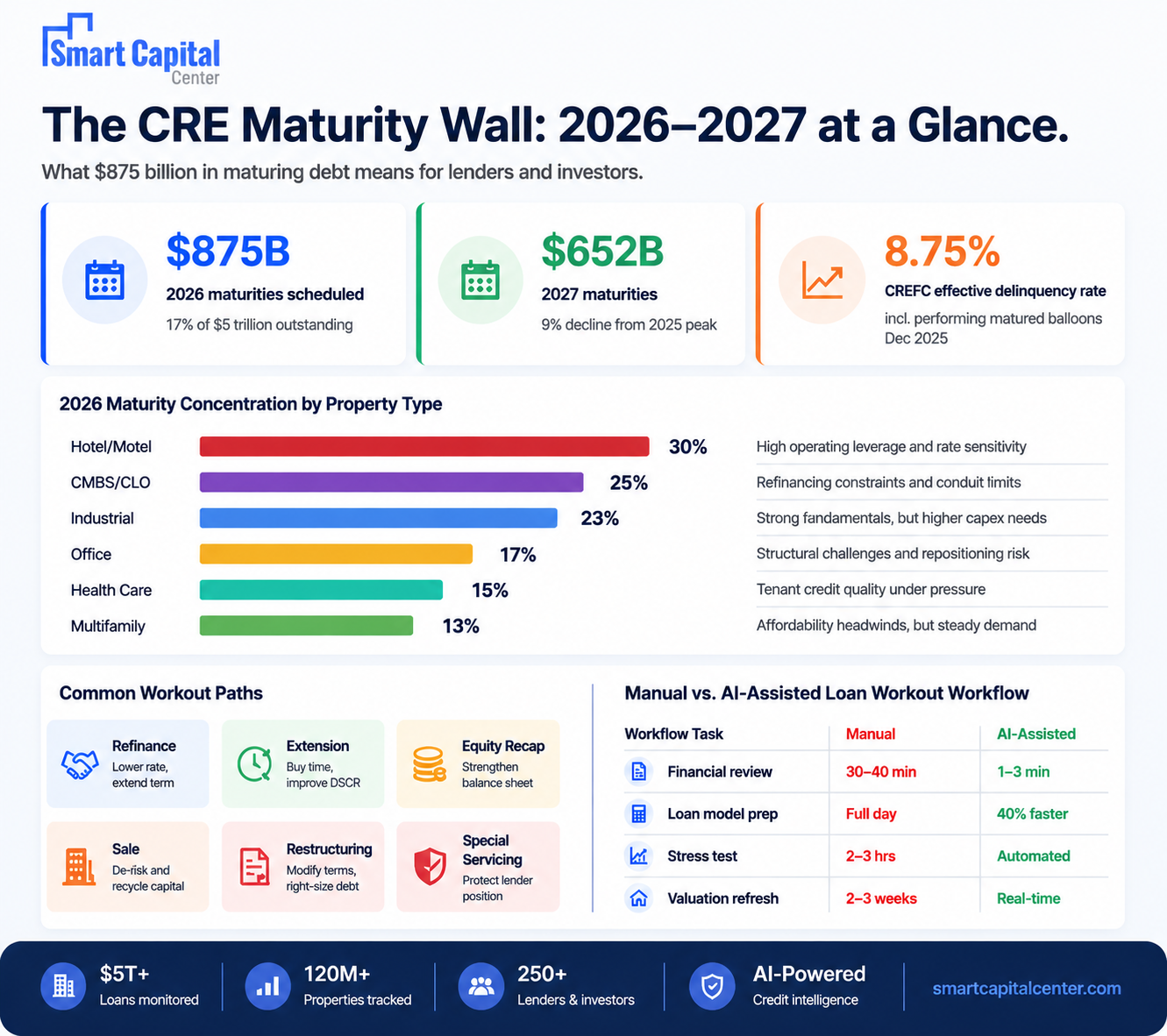

According to the MBA’s 2025 Commercial Real Estate Survey of Loan Maturity Volumes, released at the 2026 CREF Convention in San Diego, 17% of the $5 trillion of outstanding commercial mortgages, $875 billion, is scheduled to mature in 2026, with $652 billion following in 2027. “While commercial mortgage maturities remain elevated in 2026, the 9% decline from 2025 suggests that the market is beginning to move past the peak of the maturity wave in recent years,” said Reggie Booker, MBA’s Associate Vice President of Commercial/Multifamily Research. For lenders and investors carrying legacy portfolios, those figures are an operational planning mandate.

This analysis draws on Smart Capital Center, a CRE AI platform that has processed $500B+ in transactions across 120M+ properties, used by institutional lenders, including KeyBank and asset managers, including JLL, to map how relationship lenders and institutional investors should approach the CRE maturity wall before it becomes a capacity crisis.

The CRE debt maturity wall is the result of multiple overlapping loan cohorts (five-year and ten-year paper) reaching their expiration dates simultaneously in a rate environment that has changed materially since origination. Loans written at pandemic-era rates and 2020–2022 valuations are now maturing into a world where interest rates are structurally higher, cap rates have expanded across most asset classes, and refinancing assumptions built into the original underwriting no longer hold.

The structure of the wall matters. MBA’s Chief Economist Mike Fratantoni noted at the 2026 CREF Convention: “The data from this survey show that 2025 was a transition year, with the maturity wall shrinking after several years where the wall of scheduled maturities had been increasing. Even though longer-term interest rates were little changed over the course of the year, lenders were no longer simply extending loan terms. $875 billion in scheduled maturities in 2026 and $652 billion in 2027 will fuel additional lending activity.” The implication for portfolio managers: the window for orderly resolution is narrowing.

What has amplified the wall is a pattern of accumulated extensions. Many loans that would have matured in 2023 and 2024 were pushed forward 12 to 24 months while borrowers and lenders waited for rate stabilization. That delay strategy bought time. It also concentrated maturities into a shorter window, compressing the triage period that lenders now face.

The commercial real estate maturities in 2026 are not evenly distributed. According to the MBA’s 2025 Loan Maturity Volumes survey, the property-type breakdown reveals where stress is most concentrated:

Office carries the most headline risk because of the structural NOI problem: vacancy rates remain elevated across most major markets and the income supporting pre-pandemic underwriting assumptions has not recovered. Industrial is less distressed operationally but faces its own repricing dynamic as the 2021–2022 leasing boom assumptions meet a softer absorption environment. Multifamily loans originated in 2021 and 2022 face the sharpest rate gap: many were written at sub-4% rates on assets that would now refinance at 6%+ – a spread that either forces new equity or extends the timeline.

The structural challenge in the CRE loan maturity wall is the gap between what those loans were underwritten to and what the current financing market will support. A loan originated in 2020 at a 3.5% coupon on a multifamily asset valued at a 4.5% cap rate faces a refinancing environment where the coupon is closer to 6.25% and the applicable cap rate has expanded to 5.5%–6.0%. The resulting LTV on refinancing, against a value that may have declined 15–25% from origination, often requires the borrower to bring new equity to maintain the same debt level.

For lenders, that equity gap has a direct credit implication. A borrower who cannot bring the required equity faces three paths: a negotiated extension, a restructuring that reduces the principal, or a sale. Each of those outcomes requires a different lender workflow. The institution that treats all three the same way, queuing them in a standard maturity review process, is creating bottlenecks that compound as volume builds. According to CREFC’s December 2025 Monthly CMBS Loan Performance Report, effective delinquency rates, including performing matured balloons, reached 8.75% in late 2025, with CREFC noting that extension and modification activity was masking underlying refinancing stress. That stress is now moving from “deferred” to “due.”

Each workout path consumes different team resources, different timelines, and different data requirements. A lender managing 200 maturing loans in the next 18 months with a team sized for 60 is making a capacity problem.

The institutions managing the maturity wall most effectively are those that started 18 months before the maturity date. The conversations that produce refinancing solutions, structured extensions, and orderly sales require time. The conversations that produce distressed sales and special servicing transfers begin too late.

Three capabilities define the difference between proactive and reactive maturity management:

• Portfolio stress testing against rate, vacancy, and valuation scenarios: Every maturing loan should be modeled against three scenarios: base case, rate stress, and value stress before the borrower conversation begins. Most teams still do this manually, which limits the number of loans that can be stress-tested in a given period. Smart Capital Center automates this across the full portfolio, delivering scenario outputs against 1B+ real-time market signals without additional analyst hours.

• Early borrower outreach with structured response tracking: The ‘wait and see’ borrower pattern is the most common friction in maturity management. Borrowers who are uncertain about their refinancing path defer the conversation, and lenders who manage outreach over email lose visibility into whether the borrower responded, what they said, and what the next step is. AI-powered borrower communication tracks outreach and responses against the loan record, so no conversation falls through the cracks of a personal inbox.

• Real-time valuation refreshes to replace stale appraisals: A two-year-old appraisal in a market where cap rates have expanded 100 basis points is a liability in a refinancing conversation. Smart Capital Center’s real-time market intelligence, drawing on 120M+ properties and live transaction data, provides current valuation context before the borrower sits down at the table.

The CRE maturity wall 2026 is widely discussed as a credit problem. It is underappreciated as a capacity problem. A portfolio manager carrying 200 loans with staggered maturities through 2026 and 2027 does not have a different credit exposure than their team had before. They have a different workload. Every maturing loan requires a financial statement review, a current market valuation, a borrower outreach sequence, a workout path determination, and, if a modification or extension is warranted, a credit memo package. At three loans per week, a single analyst is at capacity. At twelve, the queue collapses.

KeyBank documented a 40% reduction in loan model preparation time after deploying Smart Capital Center. JLL achieved a 30x productivity gain in financial statement processing, compressing per-document time from 30–40 minutes to under three minutes. Neither result came from hiring. Both came from eliminating the manual extraction and reconciliation steps that consume the first analyst day on every new review cycle. At CRE debt maturity volumes of $875B in 2026 and $652B in 2027, the capacity math matters as much as the credit math.

A loan current on payments but past its maturity date occupies a grey zone that regulatory examiners increasingly scrutinize. CREFC’s December 2025 data showed effective delinquency rising to 8.75% when performing matured balloons are included. For lenders with significant volumes in this category, the risk is the aggregate examiner's conclusion about loan monitoring discipline across the portfolio.

Smart Capital Center mitigates this through continuous portfolio monitoring that surfaces maturity risk signals 18 months in advance, with automated borrower outreach that is logged against the loan record and configurable alerts when borrowers have not responded within defined windows.

Office and multifamily valuations in many markets have moved 15–25% from 2022 peaks. A lender entering a modification or extension discussion with origination-era collateral values is negotiating against an anchor that no longer reflects the market. The borrower knows it. If the lender’s credit team has not refreshed collateral values before the conversation, they lose control of the negotiating frame before it starts.

Smart Capital Center mitigates this through real-time valuation refreshes that draw on 1B+ live market signals across 120M+ properties, providing current collateral context before any modification or refinancing discussion begins.

When loan volume exceeds analyst capacity, the natural response is to triage informally: the noisiest loans get attention, the quiet ones get deferred. In a maturity workout context, quiet often means a borrower who has stopped responding. Inconsistent triage at portfolio scale produces the examiner’s least favorite outcome: uneven application of credit standards across comparable situations.

Smart Capital Center mitigates this through automated financial statement processing, portfolio-level stress testing, and AI-generated credit memo drafts that allow the same team to maintain consistent analytical standards across 3x the loan volume, without adding headcount.

1. Step 1: Pull your full maturity schedule 24 months forward and segment by workout risk. Map every loan by maturity date, current LTV, DSCR at origination vs. current, and borrower communication history. This baseline is triage preparation. Smart Capital Center delivers this view across the full portfolio instantly, without a manual spreadsheet assembly cycle.

2. Step 2: Run a three-scenario stress test on every loan maturing in the next 18 months. Model each loan against a base case, a 100-basis-point rate increase, and a 15% value decline. Loans that cannot support debt service under the stress scenarios are your priority outreach list. Smart Capital Center automates this against real-time market signals.

3. Step 3: Initiate structured borrower outreach 18 months before maturity, not 90 days. The most productive modification and extension conversations happen when the borrower has time to explore options. Conversations that begin at 90 days are reactive by definition. Configure automated outreach through Smart Capital Center’s portal, with every response logged against the loan record and routed to the appropriate team member.

4. Step 4: Refresh collateral valuations before any modification or extension discussion begins. Replace origination-era appraisals with current market intelligence before the borrower sits across the table. Smart Capital Center’s real-time market signals provide current comp-based valuation context for every property in the portfolio without waiting for a third-party appraisal cycle.

5. Step 5: Generate credit memo drafts from updated underwriting data instead of blank templates. Every extension, modification, or restructuring requires a credit package. At maturity volumes of 200+ loans, building each from scratch is a capacity constraint. Smart Capital Center generates credit memo drafts from underlying underwriting data in minutes, with customizable templates that match your committee’s format and standards.

The institutions that manage the CRE maturity wall without portfolio-level impairment are those whose operational infrastructure allowed them to identify risk early, engage borrowers before positions hardened, and process workout volume without sacrificing credit standard consistency.

Smart Capital Center’s continuous portfolio monitoring, automated borrower communication, real-time valuation refreshes, and AI-generated credit packages give relationship lenders and institutional investors the capacity to manage the CRE loan maturity wall at scale, without hiring ahead of a cycle that may not produce the origination volume to justify it.

Catch maturity risk 18 months out, not 30 days before the conversation you needed to start last year. Book a demo with Smart Capital Center.

According to the MBA’s 2025 Commercial Real Estate Survey of Loan Maturity Volumes, released at the 2026 CREF Convention, $875 billion in commercial mortgages – 17% of the $5 trillion outstanding – is scheduled to mature in 2026, followed by $652 billion in 2027. These figures include loans across depositories, CMBS, life insurance companies, debt funds, and agency lenders. The 2026 total represents a 9% decline from the $957 billion that matured in 2025, suggesting the peak of the commercial real estate loan maturity wave is beginning to pass, but the volume that remains requires active management.

The highest-risk positions in a CRE maturity wall context are loans where three conditions overlap: the loan matures within 18 months, the origination-era DSCR has deteriorated based on current financials, and the current market value of the collateral has declined from the origination appraisal. Loans that meet all three criteria are refinancing candidates who cannot refinance at par without new equity. Smart Capital Center’s portfolio monitoring layer flags this combination automatically, drawing on 1B+ real-time market signals and continuous financial statement analysis, without requiring a manual review cycle to surface the risk.

Lender teams managing CRE debt maturity effectively consistently report that the productive conversations began 18 months before the maturity date. At 90 days, borrowers who cannot refinance are already in a defensive position, and lenders have fewer leverage points to structure a workout that protects collateral value. The 18-month window gives both parties time to explore options, source capital, and negotiate terms without the pressure of an imminent default. Smart Capital Center’s automated outreach system initiates structured borrower communication on your defined schedule, tracks every response against the loan record, and alerts your team when a borrower has gone silent.

Portfolio stress testing for commercial real estate maturities requires modeling each loan against multiple rate, vacancy, and valuation scenarios – a process that, done manually, consumes 2–3 hours per loan. For a 200-loan portfolio, that is 400–600 analyst hours before any workout decisions have been made. Smart Capital Center automates multi-scenario stress testing against real-time market inputs, compressing what was a multi-day analyst project into a platform-generated output that the team can act on immediately. The same tool that surfaces the stress scenario also flags which loans require priority attention based on the depth of the shortfall.

When a borrower cannot refinance a maturing commercial real estate loan at current market rates, the viable paths are: a negotiated extension with reset covenants and an active monitoring plan; a structured modification that adjusts the loan terms to align with current debt service capacity; a recapitalization in which the borrower brings new equity or a joint venture partner to close the refinancing gap; or a managed sale that preserves collateral value rather than triggering a distressed disposition. The worst outcome for both borrower and lender is a conversation that starts too late for any of these options to be executed with adequate lead time. The CRE maturity wall makes early triage not a best practice but an operational requirement.

AI addresses the CRE maturity wall on three dimensions simultaneously: it compresses the time required to process financial statements and generate updated underwriting models (KeyBank achieved a 40% reduction in loan model preparation time; JLL achieved a 30x productivity gain in financial statement processing); it automates borrower outreach and tracks responses against the loan record so no conversation falls through an inbox; and it provides real-time portfolio valuation context that replaces stale appraisals before modification or extension discussions begin. The net effect is that the same credit team can handle materially more maturing loans without sacrificing the analytical standard that each workout decision requires. Smart Capital Center delivers all three capabilities in a single platform, integrated with the loan servicing and accounting systems institutional lenders already operate.