AI in Commercial Real Estate

July 30, 2026

AI in Commercial Real Estate

July 30, 2026

According to CBRE’s H2 2025 Cap Rate Survey, the spread between cap rates for Class A and Class B/C assets reached near-record levels in the second half of 2025 – a market condition where a 25-basis-point error in underwriting assumptions for the wrong asset tier produces materially mispriced deals. In a flat market, assumption errors are recoverable. In a market defined by dispersion and rapid submarket divergence, they compound. For an investor or lender, applying a 3.5% rent growth convention to a market running at 1.2% without validation is a bet.

This analysis draws on Smart Capital Center, a CRE AI platform validating underwriting in commercial real estate against 1B+ real-time market signals across 120M+ properties, used by institutional investors and lenders including JLL and KeyBank, to map how AI-powered assumption validation works and where it catches what manual review misses.

Underwriting assumptions are the forward-looking inputs that drive every CRE financial model. They are projections grounded in market data, analyst judgment, and convention. The primary assumptions in any commercial deal include:

• Rent growth rate: The projected annual increase in effective rent over the hold period, applied to current in-place rents and vacancy absorption assumptions.

• Vacancy and absorption: The stabilized occupancy rate the model targets and the time assumed to reach it, both of which drive revenue projections in the critical early years.

• Exit cap rate: The capitalization rate applied to terminal NOI to establish disposition value – the single assumption with the highest sensitivity in most hold-period return models.

• Expense ratios and management fees: Operating expense benchmarks, CAM recovery assumptions, and property management fee structures that determine NOI from a given revenue line.

• Debt service coverage: The DSCR threshold that determines whether the deal can support the proposed financing structure across the hold period, including under stress scenarios.

In practice, these assumptions are set through a combination of analyst experience, the most recent available market report, a manually pulled comp set, and institutional convention. Each of those sources carries lag, selection bias, or subjectivity. Applied across a growing portfolio, the aggregate effect of small individual assumption errors becomes a systemic exposure.

A single deal underwritten with a rent growth assumption 100 basis points above market is a pricing error. The same assumption applied across 40 acquisitions in a three-year deployment cycle is a portfolio-level impairment waiting to materialize. Analysts do not set wrong assumptions intentionally. The validation step takes long enough that it gets abbreviated or skipped when deal volume is high.

According to Trepp’s Q4 2024 CRE Loan Performance Report, a significant share of CRE loan losses in the 2023–2025 period traced to underwriting models built on rent growth and vacancy assumptions that were not validated against transaction-level submarket data at the time of origination, and that diverged materially from actual market conditions within 18 months of closing. The origination-era models were simply unvalidated against the specific conditions of the specific submarket.

The compounding problem is temporal: assumptions set at origination are rarely re-examined systematically during the hold period unless a trigger event forces it. A property whose financials have drifted materially from its underwriting model six quarters after closing is carrying variance no one is tracking.

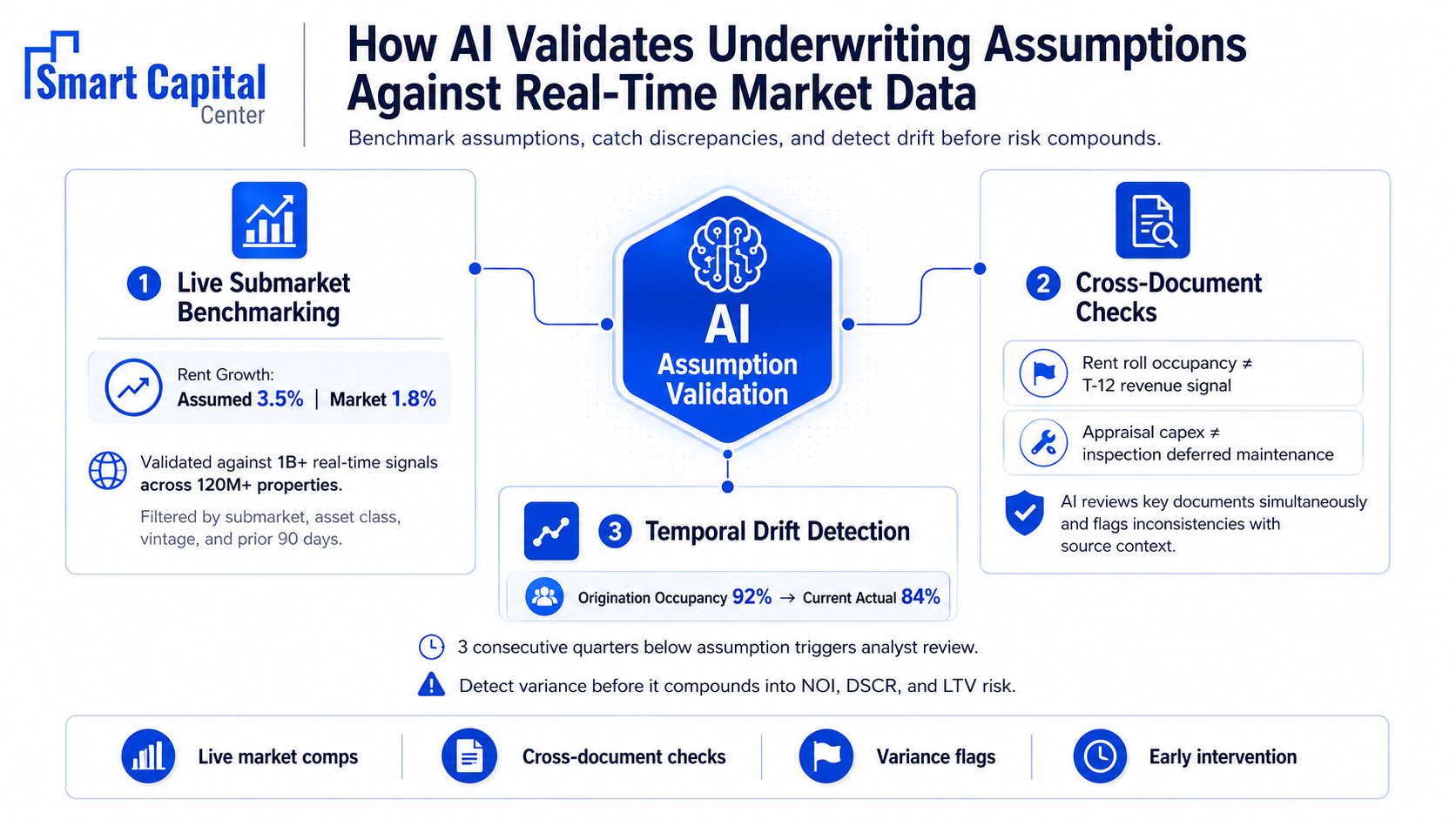

Smart Capital Center’s AI analysts validate underwriting assumptions against 1B+ real-time market signals spanning 120M+ properties. For a rent growth assumption, this means comparing the model input against actual executed lease transactions in the same submarket, asset class, and vintage range, filtered to the prior 90 days. A 3.5% rent growth assumption in a market where executed transactions show 1.8% average effective rent growth over the prior two quarters is flagged immediately, with the specific comp set that generated the variance cited as the source.

The same logic applies to vacancy assumptions. Rather than accepting a stabilized occupancy target of 94% at face value, the AI cross-references current absorption rates, active listings, and lease expiration data in the submarket to assess whether 94% is achievable within the model’s assumed lease-up timeline.

Manual underwriting reviews documents sequentially. AI reviews them simultaneously and cross-references them structurally. This is where a category of assumption errors surfaces that sequential review almost never catches: inconsistencies between the assumption stated in the model and the data present in the deal’s own supporting documents.

Smart Capital Center flags these cross-document inconsistencies automatically:

• An appraisal capex assumption that does not match the inspection report’s deferred maintenance estimate

• A rent roll occupancy rate that contradicts the T-12 revenue line after accounting for stated concession periods

• A management fee in the OM pro forma that exceeds the executed property management contract on file

• A stated expense ratio that falls materially below what the trailing twelve months of actuals show for the same property

Each inconsistency is flagged with the specific documents on both sides of the conflict and a brief AI-generated explanation of the discrepancy. For example, “a zoning change in Q3 2024 drove a 22% tax assessment increase that is not reflected in the OM expense assumption.” The analyst sees the variance, the reasoning, and the source in one view.

Assumption validation is an ongoing portfolio management requirement. According to McKinsey’s 2025 AI Survey, AI-powered variance detection identifies assumption drift in financial models at rates significantly higher than periodic manual review cycles, because AI monitors continuously rather than quarterly, and because it compares current data against origination-era assumptions systematically rather than selectively.

Smart Capital Center’s temporal drift detection flags when a property’s current financials have diverged materially from the assumptions embedded in the original underwriting model. A property underwritten to 92% occupancy that has run at 84% for three consecutive quarters is carrying an assumption variance that compounds in NOI, DSCR, and LTV calculations until it is addressed. The AI surfaces this before it reaches a covenant breach or a credit review, giving the analyst and the lender the intervention window.

A lender or investor using a 3% rent growth convention in an industrial submarket that absorbed 40 million square feet of new supply in 2024 is modeling a future that the market has already moved away from. The assumption is not wrong in principle. It reflects a reasonable long-run average. It is wrong for this submarket, at this moment, and it produces an NOI projection that overstates stabilized income by a margin that shows up in DSCR and LTV calculations.

Smart Capital Center mitigates this through live submarket rent comp benchmarking that compares model inputs against executed transactions in the specific submarket within the prior 90 days, flagging divergences between the assumed growth rate and the rate the market is producing.

An appraisal that assumes $2.50 per square foot in annual capex and an inspection report that documents $4.80 per square foot in deferred maintenance represent a material assumption gap in a refinancing model. A reviewer reading each document in sequence may note both figures without connecting them. AI identifies the conflict in real time, across both documents simultaneously.

Smart Capital Center mitigates this through automated cross-document consistency checks that compare assumptions and figures across all deal documents simultaneously, flagging conflicts with the specific source documents on both sides of the discrepancy and AI-generated reasoning about what drove the gap.

1. Step 1: Establish a comp-set definition standard before validating any assumption. Specify the submarket boundary, asset class, vintage range, and transaction recency threshold that make a comparable genuinely applicable to the subject property. Validating a rent growth assumption against a metro-level average when the subject is in a specific industrial corridor produces a benchmark that conceals the local variance the validation is meant to surface.

2. Step 2: Run cross-document consistency checks before the model is finalized. Before any underwriting model leaves the analyst’s desk, verify that key assumptions are consistent across the OM, appraisal, rent roll, T-12, and inspection report. Document every inconsistency and its resolution. Smart Capital Center automates this step, surfacing conflicts across all deal documents simultaneously with AI-generated variance commentary.

3. Step 3: Build temporal monitoring into the portfolio framework. Set assumption variance thresholds – occupancy more than 5 percentage points below underwriting, NOI more than 10% below model, submarket rent growth more than 150 basis points below origination assumption – and configure automated alerts when properties cross them. Assumption validation that ends at closing is not portfolio risk management.

4. Step 4: Benchmark new deals against your own portfolio’s real financials. Smart Capital Center builds a proprietary benchmark database from every document analyzed on the platform, allowing firms to compare new deal assumptions against actual performance data from their own analyzed deals in comparable markets and asset classes. This proprietary layer is more accurate for your specific deal universe than any third-party source alone.

The models that fail are the ones with right calculations applied to unvalidated assumptions, where the math is correct, and the inputs are wrong, and no one in the review process had the data or the time to catch the divergence.

Smart Capital Center’s AI validation layer benchmarks every material underwriting assumption against 1B+ real-time market signals, runs cross-document consistency checks across every deal package simultaneously, and monitors for temporal drift between origination-era assumptions and current property financials. Every flagged variance links back to the data or document that triggered it, giving analysts the reasoning they need to investigate.

See how Smart Capital Center validates your underwriting assumptions against live market data, on a deal from your own pipeline. Book a demo today.

Underwriting assumptions are the forward-looking inputs that drive every CRE financial model. Underwriting assumptions are projections, and the accuracy of every output in the model depends on how well they reflect current market conditions in the specific submarket and asset class being analyzed. A model with correct calculations but unvalidated assumptions produces outputs that look rigorous while resting on inputs that may be materially wrong. At portfolio scale, commercial real estate valuation errors that appear small on individual deals become a systemic exposure over time.

Manual assumption validation requires an analyst to pull comps from one system, cross-reference them against the model inputs in another, and flag divergences from memory or by side-by-side comparison. AI validates assumptions by simultaneously benchmarking every material input against real-time market data and running cross-document consistency checks across the full deal package in parallel. Smart Capital Center surfaces variances with AI-generated reasoning and source citations, so the analyst sees why and which data triggered the flag.

A cap rate assumption is defensible when it is grounded in closed transactions in the specific submarket and asset tier of the subject property, updated within the prior 90 days. According to CBRE’s H2 2025 Cap Rate Survey, the spread between Class A and Class B/C asset cap rates reached near-record levels in 2025, making blended-market averages misleading for asset-tier-specific underwriting. Smart Capital Center benchmarks exit cap rate assumptions against transaction-validated data by submarket and quality tier, flagging divergences from market-current levels with the specific comp set that generated the variance.

Temporal drift detection compares current property financial data against the assumptions embedded at origination on a continuous basis rather than at periodic review intervals. When a property’s actual occupancy, NOI, or expense ratio has moved materially from the underwriting model, the AI flags the variance and surfaces the magnitude of the gap. Smart Capital Center’s monitoring layer does this automatically across the full portfolio, giving lenders and asset managers the intervention window before a drifted assumption triggers a covenant breach or credit review.

The four elements of a scalable validation process are: a defined comp-set standard that specifies the geography, asset class, vintage, and recency of comparables used for each assumption type; automated cross-document consistency checks run before any model is finalized; portfolio-level temporal monitoring with configured variance thresholds that trigger alerts rather than waiting for periodic review; and a proprietary benchmark layer built from your own analyzed deals rather than relying solely on third-party data. Smart Capital Center automates all four elements, with every flagged assumption linking back to the source data or document that triggered the flag.