AI in Commercial Real Estate

June 30, 2026

AI in Commercial Real Estate

June 30, 2026

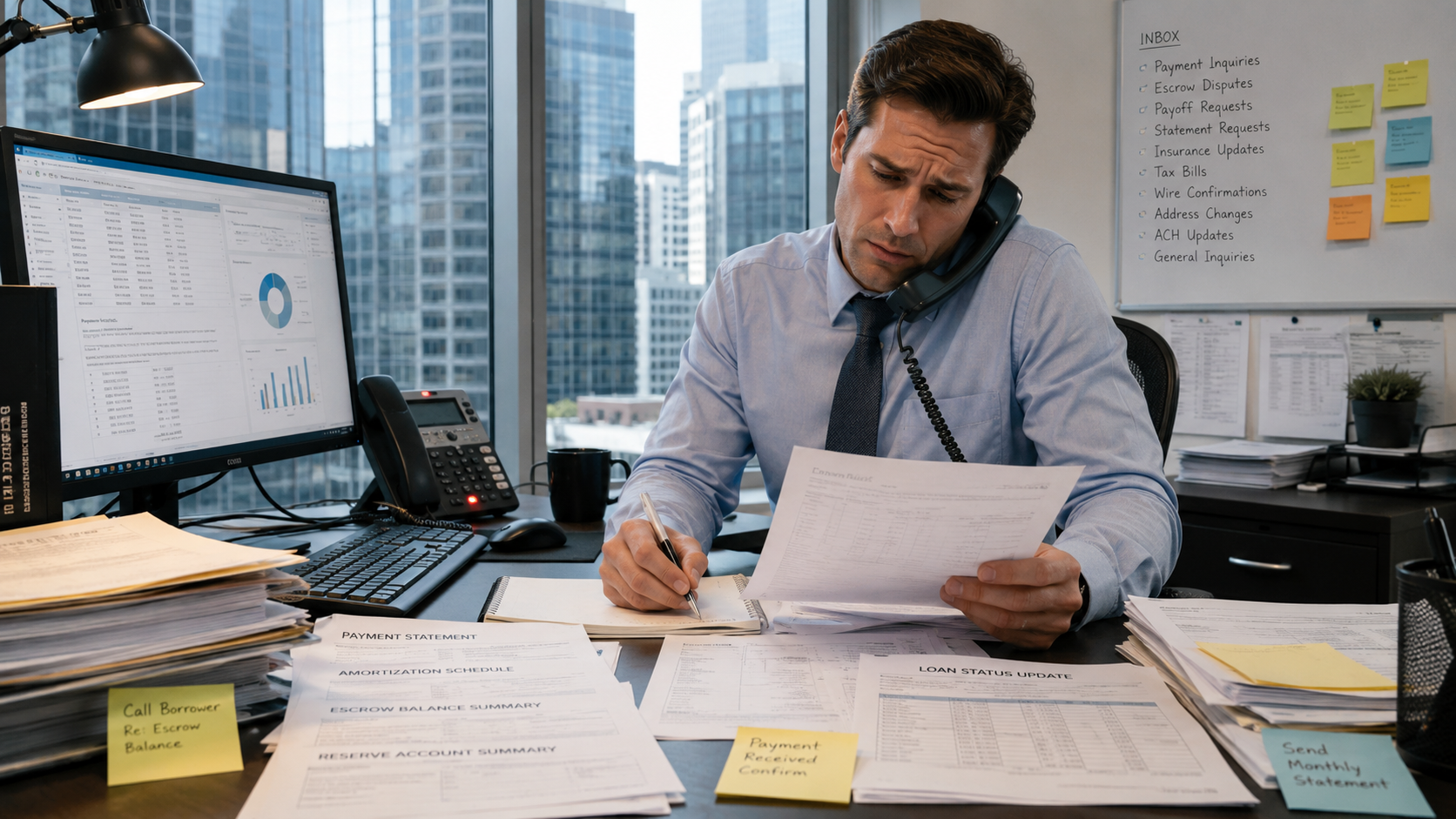

According to Deloitte’s 2026 Banking and Capital Markets Outlook, operational efficiency in loan servicing is now a top-three cost management priority for commercial lenders, with manual borrower communication handling identified as one of the highest-volume, lowest-value drains on loan servicing team capacity. For commercial real estate loan servicing teams managing portfolios of 100 loans or more, the math is direct: if the average borrower query takes 15 minutes to handle manually and each loan generates two routine queries per month, a 200-loan portfolio is consuming over 100 analyst hours per month on questions that a self-service portal answers in seconds.

This analysis draws on Smart Capital Center, a CRE platform processing $500B+ in analyzed transactions across 120M+ properties, used by institutional lenders including KeyBank, to map how a borrower portal restructures commercial loan servicing workflows and where the measurable cost reductions appear.

The hidden cost of loan servicing comes from routine queries: payment statements, amortization schedules, escrow balances, reserve account summaries, and loan status updates. These questions are answerable, answerable quickly, and asked repeatedly by every borrower in the portfolio.

At a portfolio of 150 loans, a team handling two routine borrower queries per loan per month is fielding 300 inbound requests. At 15 minutes each, that is 75 hours of loan servicing capacity consumed by questions that carry zero analytical value. Multiply by all-in labor cost and the annual figure runs well into six figures for a mid-sized portfolio for work that produces no credit insight, no relationship value, and no regulatory output.

The same pattern appears in document exchange. Financial statement submissions, repair authorization requests, and escrow disbursement approvals that travel over unencrypted email require manual tracking, manual filing, and manual follow-up when submissions are incomplete. According to PwC’s Emerging Trends in Real Estate 2026, lenders that have automated routine borrower communication workflows are reallocating an average of 20–30% of team capacity to higher-value portfolio oversight functions, without adding staff.

The underlying cost structure of manual loan servicing is quantified in primary industry research. According to the MBA’s 2024 Servicing Operations Study and Forum, fully-loaded servicing costs for performing loans averaged $176 per loan annually. For non-performing loans, that figure rises to $1,573 per loan. The 9x cost differential between performing and distressed loan servicing underscores why early identification of at-risk positions through automated monitoring pays for itself: the cost of proactive oversight is structurally lower than the cost of reactive default management.

The compliance dimension of this shift carries its own cost logic. Atul Dubey, Executive Vice President and General Manager of Compliance Solutions at Wolters Kluwer, noted in the firm’s Q1 2026 Banking Compliance AI Trend Report: “Banks are moving quickly to embed agentic AI, potentially at the expense of clear strategy and AI governance. Our findings underscore the critical need for collaboration with regulatory and compliance experts to ensure that strategic goals, governance and transparency agendas are advanced concurrently with AI adoption at scale to drive sustainable success.” The same report found that 46.6% of financial institutions now cite operational efficiency as their primary AI and machine learning goal, with loan servicing automation consistently identified as one of the clearest ROI opportunities.

Smart Capital Center's borrower portal provides self-service access on demand, formatted consistently, and current as of the last system update. A borrower who would otherwise email the loan servicing team logs into the portal and downloads what they need in under two minutes. The team is not involved. The query never enters the inbox. Available self-service items include:

The most operationally expensive loan servicing workflows are inbound submissions: financial statements due monthly, repair authorization requests, escrow disbursement approvals, and reserve replenishment documentation. When these arrive over email, each requires manual receipt acknowledgment, routing, and follow-up if the submission is incomplete.

Smart Capital Center converts every inbound submission into a trackable portal task. The workflow for a repair reimbursement request, for example, runs as follows:

Nothing is lost in an inbox. No follow-up email is needed to confirm receipt. For a look at how this fits into a broader AI-connected lending operation, see MBA CREF 2026 Technology Council: AI and Connected Intelligence in CRE Lending.

Maturity notices, reserve replenishment reminders, financial statement due dates, and insurance renewal deadlines are events every loan generates on a predictable schedule. Managing them manually scales linearly with portfolio size: a 200-loan portfolio means 200 separate tracking threads.

Smart Capital Center's configurable notification system automates these reminders with consolidated delivery. Key features:

Every communication in a manual loan servicing workflow requires deliberate logging to produce a compliance record. In practice, this logging is inconsistent: some interactions are documented thoroughly, others are not documented at all, and reconstructing a communication history during a regulatory examination or borrower dispute requires manual search across email archives and file folders.

Smart Capital Center logs every borrower interaction automatically: portal logins, document submissions, request status changes, notification deliveries, and reviewer actions. The full communication record is searchable, timestamped, and exportable for regulatory review, without any manual documentation effort from the team. For lenders subject to OCC, FDIC, or state regulatory examination, this loan servicing automation is a compliance benefit that manual loan servicing processes cannot replicate at the same reliability.

When borrower requests arrive over email, phone, and portal simultaneously with no unified tracking system, the loan servicing team handles each through whatever channel it arrived. Some interactions are documented; many are not. A borrower dispute about a payment application or a missed maturity notice becomes difficult to resolve when the communication record is fragmented across personal inboxes and paper notes.

Smart Capital Center mitigates this through a unified communication layer where every borrower interaction, regardless of whether it originated in the portal or arrived by email, is logged, timestamped, and searchable. Borrowers who prefer email still fit the workflow; their submissions are converted into tracked portal tasks rather than lost in an inbox thread.

Financial statements, rent rolls, tax returns, and insurance documents routinely travel over unencrypted email in standard loan servicing workflows. For lenders subject to data security requirements under GLBA, state privacy laws, or institutional policy, this exposure is both a regulatory risk and a reputational one. A single inadvertent email to the wrong recipient containing borrower financial data creates an incident that manual workflows have no mechanism to prevent.

Smart Capital Center mitigates this through secure document exchange through the borrower portal, replacing unencrypted email transmission with an encrypted, access-controlled submission channel. Every document uploaded through the portal is stored securely, access-logged, and retrievable for compliance review, eliminating the transmission risk that email-based document exchange introduces.

Before committing to a borrower portal, run it against the four criteria that determine whether it reduces loan servicing costs or simply adds another system for the team to manage.

Every routine borrower query handled manually is an hour of capacity given up to routine work. At portfolio scale, that cost is a real drag on team capacity to do the work that requires judgment.

Smart Capital Center’s borrower portal converts commercial real estate loan servicing from a reactive, inbox-driven function into a structured, self-service operation, with every interaction logged, every document tracked, and every notification automated. The loan servicing team handles what requires human review. Everything else handles itself.

Cut routine loan servicing queries and free your team for the work that requires judgment. Book a demo with Smart Capital Center.

A borrower portal eliminates the team’s involvement in routine queries by giving borrowers direct, self-service access to the information they would otherwise request by email or phone. Payment statements, amortization schedules, escrow balances, and loan status updates are available on demand through the portal, without requiring a team member to locate, format, and send each one. At a 200-loan portfolio with two routine queries per loan per month, the time savings runs to over 100 analyst hours monthly – capacity that can be redeployed to portfolio oversight and relationship management rather than statement retrieval.

The highest-volume routine requests are payment statements, amortization schedules, escrow balance summaries, debt-service breakdowns, and loan status updates. These requests are answerable, consistent in format, and asked repeatedly across every borrower in the portfolio, making them the highest-value candidates for self-service automation. Smart Capital Center’s loan management software provides instant access to all of these, converting what is currently a manual, email-driven process into a zero-touch self-service function.

The risk with email-based document submission is exactly what the question implies: submissions arrive in personal inboxes, acknowledgment depends on the individual who happens to see it first, and follow-up when submissions are incomplete requires manual tracking. Smart Capital Center converts every inbound borrower submission into a tracked portal task with automatic routing to the appropriate team member, a logged receipt timestamp, and a status trail that shows every action taken from submission to resolution. Nothing is lost between channels, and the audit record is generated automatically without requiring manual documentation.

The compliance benefit is structural: every borrower interaction logged automatically, without relying on individual team members to document their communications consistently. Smart Capital Center’s portal logs logins, document submissions, request status changes, notification deliveries, and reviewer actions, with timestamps and exportable records for regulatory review. For lenders subject to OCC, FDIC, or state examination, this replaces the manual log reconstruction that audits currently require with a system-generated record that is always current and always complete.

Borrowers managing multiple properties under the same lender relationship do not want a separate email for every maturity notice, reserve reminder, and financial statement due date across each loan. Smart Capital Center delivers consolidated notifications that aggregate all relevant upcoming dates and required actions into a single communication per borrower, reducing both inbound borrower confusion and the ops burden of managing separate notification threads per property. Configurable reminder schedules mean the loan servicing team sets the parameters once, and the system handles delivery automatically across the portfolio.