CRE Lenders

July 13, 2026

CRE Lenders

July 13, 2026

.jpg)

Most commercial real estate lenders are data-rich but intelligence-poor. They have access to enormous volumes of loan documents, borrower financials, rent rolls, and market data — but lack the connected infrastructure to turn that information into faster, more confident decisions.

According to Deloitte's 2026 Commercial Real Estate Outlook, more than 60% of CRE finance organizations cite data fragmentation and manual reconciliation as their primary barriers to operational efficiency. That gap between data availability and connected intelligence was the central insight driving discussion at the MBA CREF 2026 Technology Council.

At a council session following the MBA CREF 2026 convention, technology leaders, lenders, and industry experts gathered to explore how artificial intelligence, automation, and digital knowledge systems are transforming commercial real estate lending operations.

As part of the session, Laura Krashakova, CEO of Smart Capital Center, discussed how modern data infrastructure and AI can connect fragmented information across underwriting, asset management, reporting, loan documentation, insurance compliance and hundreds of other workflows, — giving lenders a centralized intelligence layer for stronger portfolio decision-making.

At the event, Smart Capital Center presented how its AI platform addresses data fragmentation across the full CRE loan lifecycle — backed by $500B+ in analyzed transactions, 120M+ properties, and clientsincluding KeyBank, JLL, and The RMR Group.

One example of the connected intelligence layer in action: Smart Capital Center recently launched a Fraud Alert capability for lenders and servicers — detecting inconsistencies across documents and data sources in real time, surfacing early warning signals for potential fraud before they become exposure.

A direct application of what connected workflows make possible: CRE finance organizations that are more intelligent, more efficient, and more proactive across the full loan lifecycle.

The MBA Technology Council provides a space for professionals across the industry to share insights and discuss how technological change is affecting commercial real estate finance operations. Opening the session, council leadership highlighted how recent industry events and conferences have reinforced several recurring themes that technology leaders are actively addressing today.

Among the most prominent topics across the industry are:

These topics reflect a broader shift occurring across CRE finance organizations. Over the past decade, lenders have digitized many aspects of their operations. However, digitization alone does not necessarily translate into improved decision-making.

Many firms today have access to enormous amounts of data. The challenge is how to connect that information in ways that provide meaningful, actionable insight — and that is precisely where the council's discussion focused.

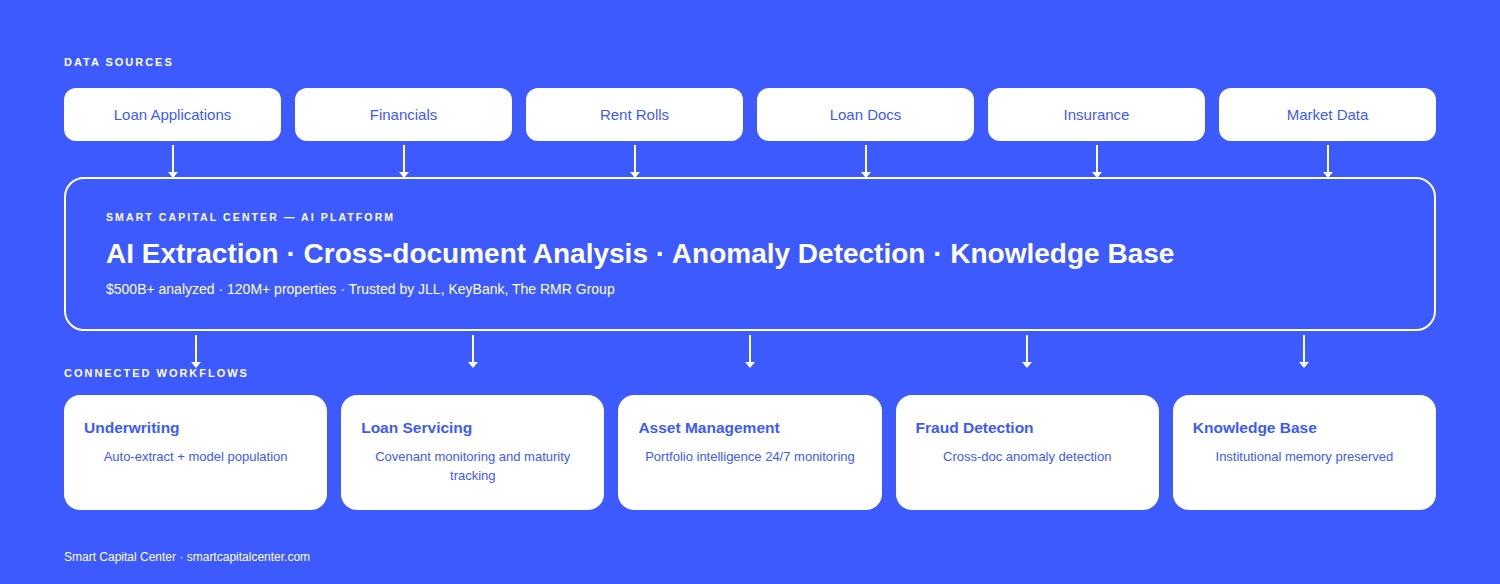

One of the central ideas discussed during the council meeting was the gap between data availability and connected intelligence. Commercial real estate finance generates an immense amount of documentation and operational information across the life cycle of a loan — produced during origination, underwriting, closing, servicing, and asset management.

Examples of these data sources include:

Although this information exists within most organizations, it is often distributed across different systems, teams, and workflows. Important information may exist somewhere within the organization, but it is difficult to access, difficult to cross-reference, and rarely used as part of a broader analytical framework.

For many years, operational workflows in CRE lending have been organized around separate functions.

Each team maintains its own documentation, data, and systems.

While these functions are essential, they are often only loosely connected.

As a result, valuable data remains fragmented across systems and teams.

Artificial intelligence and modern data infrastructure are beginning to change this model. New systems can extract structured information from a wide range of documents and operational data sources. Once captured, this information can move across workflows rather than remaining tied to a single stage of the lending process.

Artificial intelligence and modern data infrastructure are beginning to change this model. New systems can extract structured information from a wide range of documents and operational data sources. Once captured, this information can move across workflows rather than remaining tied to a single stage of the lending process.

Commercial real estate finance generates an enormous volume of information across the life of a loan — underwriting memos, borrower communications, covenant documentation, insurance reviews, financial variance analyses, and internal credit discussions. In most institutions, this information remains scattered across systems, email threads, spreadsheets, and document repositories, making it difficult to access and nearly impossible to use as part of a broader analytical framework.

Smart Capital Center addresses this directly. The platform continuously aggregates data across the full loan lifecycle, transforming fragmented information into a centralized intelligence layer that teams can activelywork with.

In practice, this means information captured during underwriting can inform asset management decisions years later. Loan agreements feed automated covenant monitoring. Insurance requirements are validateddynamically as documentation is updated. Borrower communications and servicing notes become part of a persistent institutional knowledge base rather than disappearing into inboxes or archived folders.

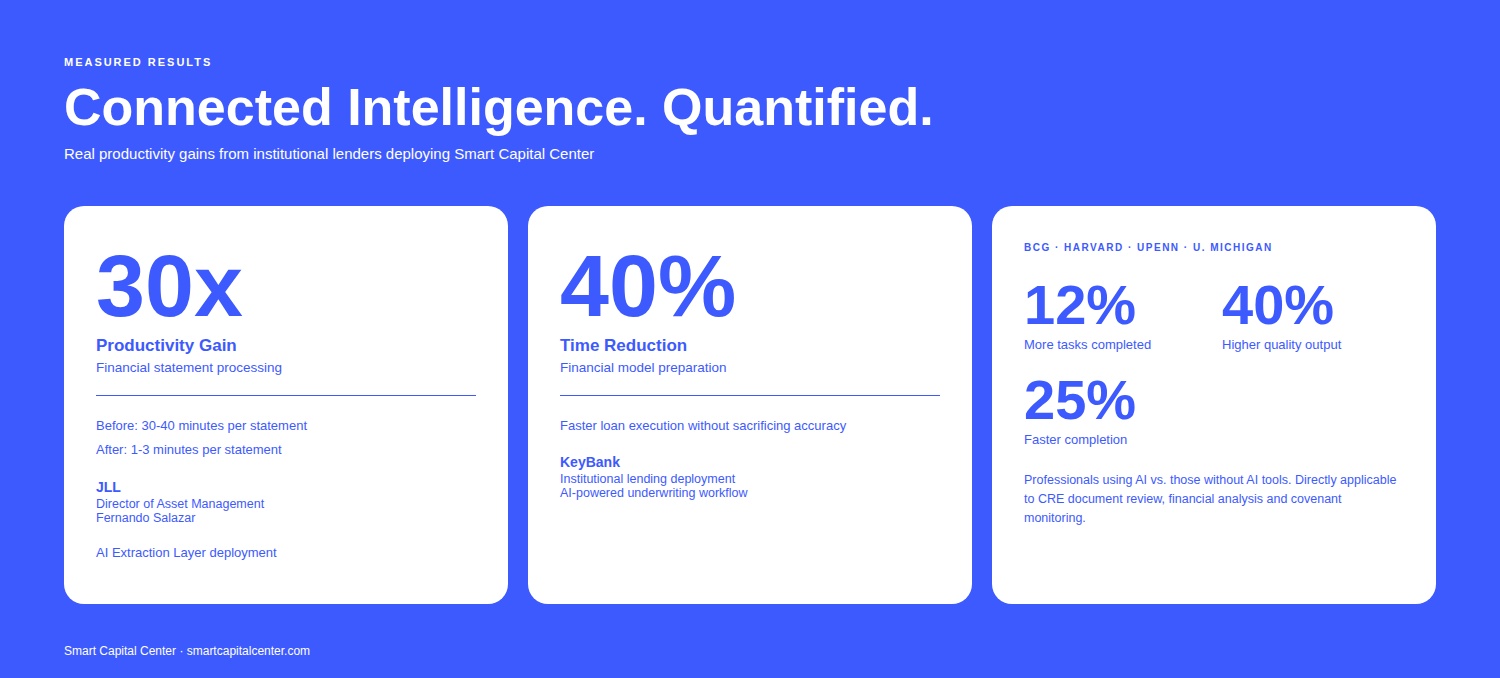

The results are measurable. Fernando Salazar, Director of Asset Management at JLL, reported that financial statement processing dropped from 30–40 minutes per statement to 1–3 minutes after deploying Smart Capital Center's AI extraction layer — a 30x productivity gain on one of underwriting's most time-consuming inputs. KeyBank achieved a 40% reduction in the time required to prepare financial models for loans, accelerating execution while maintaining accuracy.

Rather than functioning only as historical records, operational data becomes an active intelligence layer — one that continuously informs decision-making across the portfolio and helps institutions respond faster as market conditions evolve.

A key theme from the council discussion was the shift from reactive monitoring toward continuous intelligence.

Historically, many CRE institutions relied on periodic reviews, manual reconciliations, and point-in-time analysis. While effective in smaller portfolios, these approaches become difficult to scale as loan portfolios expand and data sources multiply.

Artificial intelligence allows institutions to move toward continuous anomaly detection and cross-workflow intelligence. Instead of reviewing individual documents or transactions, AI systems analyze relationships between data sources across the full lifecycle of a loan — from origination and underwriting to servicing and asset management. This shift enables lenders to detect risks earlier, maintain stronger portfolio monitoring, and operate with greater consistency across teams.

According to a Boston Consulting Group study conducted with researchers from Harvard, UPenn, and the University of Michigan, professionals using AI assistance completed 12% more tasks, finished them 25% faster, and produced outputs rated 40% higher in quality compared to those working without AI tools. In CRE lending — where document review, financial analysis, and covenant monitoring are core operational functions — those productivity gains translate directly into portfolio capacity and risk coverage.

The most powerful applications of artificial intelligence are not limited to a single task or workflow. AI becomes most valuable when integrated across the entire life cycle of a commercial real estate loan. The following framework maps AI capabilities to each stage, with specific evaluation criteria for each:

Smart Capital Center is designed to pass all five evaluation steps — with source-level traceability on every extracted figure and human-in-the-loop review requirements built into high-stakes decision workflows.

One issue discussed during the council meeting was the use of AI and automation to detect potential fraud signals in CRE lending workflows. Fraud in commercial real estate is not a new issue, but generative AI and other factors have increased its relevance in recent years.

Financial statements, rent rolls, and borrower narratives can now be generated or modified quickly in ways that appear plausible on the surface. Traditional manual review processes may struggle to identify subtle inconsistencies across multiple documents. Artificial intelligence systems can assist analysts by examining data patterns across a broader set of materials.

For example, AI tools can compare:

By analyzing information across multiple documents simultaneously, these systems can highlight inconsistencies or unusual patterns that may warrant further investigation. Importantly, participants emphasized that these technologies are designed to support analysts rather than replace them. The goal is to surface potential issues earlier and more efficiently, allowing professionals to apply their expertise where it matters most.

As AI becomes more integrated into operational workflows, transparency remains an essential requirement. Participants discussed the importance of ensuring that technology systems maintain clear traceability between insights and source documents.

When an automated system flags an issue or inconsistency, users should be able to immediately identify:

This traceability ensures that analysts retain full visibility into the decision process. It also supports compliance, audit requirements, and internal accountability.

Rather than replacing human judgment, AI systems should function as intelligence amplifiers, helping professionals review information more efficiently while maintaining control over final decisions.

Deploying AI across loan lifecycle workflows delivers significant operational benefits — but three specific risks require active management before institutions can rely on AI-generated outputs for credit decisions.

Extraction accuracy on non-standard documents. AI extraction models perform reliably on standard CRE document formats but can misread handwritten rent rolls, scanned financial statements with unusual column layouts, or documents with embedded tables in non-machine-readable formats.

Mitigation: implement a document quality check at ingestion that flags non-standard formatting for human review before AI extraction runs, rather than after outputs are generated.

Alert fatigue from misconfigured anomaly detection. If threshold parameters are set too broadly, continuous monitoring systems generate too many simultaneous notifications — causing operations teams to deprioritize genuine risk signals alongside false positives.

Mitigation: calibrate alert thresholds to portfolio-specific norms during a 60-day baseline period before enabling automated notifications. Smart Capital Center's configurable threshold management allows institutions to tune sensitivity by asset class and loan type.

Institutional knowledge base quality depends on data hygiene. AI-powered knowledge systems capture value only when source data is consistently structured, complete, and accurately attributed. Organizations that feed inconsistent or poorly-maintained loan files into a knowledge base will compound errors rather than eliminate them.

Mitigation: complete a data standardization audit across existing loan documentation before enabling knowledge capture features.

Smart Capital Center's extraction layer standardizes documents during ingestion, building a clean foundation for the knowledge base rather than inheriting legacy inconsistencies.

Another theme that resonated strongly during the discussion was the concept of institutional knowledge preservation. Commercial real estate organizations rely heavily on the expertise of analysts, asset managers, and other professionals who develop deep knowledge over time.

These individuals accumulate valuable insights about markets, borrowers, operational processes, and investment strategies. However, when employees transition to new roles or leave the organization, much of this knowledge can be lost.

AI-powered knowledge systems provide an opportunity to capture and retain these insights. Notes from underwriting discussions, asset management observations, and internal communications can be structured and stored within a shared knowledge base.

Even informal information, such as conference notes or internal research, can become part of an organization’s collective intelligence. Over time, this evolving knowledge base becomes an institutional asset that supports better decision-making across teams.

The ultimate impact of these technologies extends beyond individual workflows. As AI and connected data systems become more widely adopted, they are enabling a broader operational transformation across commercial real estate finance. Participants discussed several potential benefits of this transformation:

Reduced manual work: Automated data extraction and reconciliation can significantly reduce time spent on routine tasks.

Faster access to information: Centralized knowledge systems allow teams to quickly retrieve relevant documents, data, and historical insights.

Improved risk monitoring: Continuous analysis of borrower and property data can help identify emerging risks earlier.

More strategic focus: With fewer operational burdens, professionals can spend more time on strategic analysis and borrower relationships.

Stronger institutional memory: Knowledge captured across workflows becomes a durable asset that benefits the entire organization

In an industry where information complexity continues to grow, these capabilities may become critical differentiators.

As commercial real estate finance becomes increasingly data-driven, the competitive advantage for lenders will depend not only on adopting artificial intelligence tools, but also on building the data infrastructure required to support them.

Organizations that successfully connect their data across workflows will be better positioned to manage risk, improve operational efficiency, and make more informed credit decisions. The discussions at the MBA CREF 2026 Technology Council highlight that the future of CRE lending will depend on connected intelligence systems capable of transforming fragmented information into continuous, actionable insight.

Smart Capital Center is building this infrastructure today — giving lenders, investors, and asset managers the connected intelligence layer they need to operate with greater speed and confidence

For lenders, investors, and servicers alike, building this intelligence infrastructure may become one of the defining priorities of the next decade.

The Mortgage Bankers Association Technology Council convenes senior executives from the country's top commercial real estate lenders, servicers, and finance institutions for candid, peer-level dialogue on technology strategy. The council is selective by design — only a small number of technology companies are invited to present each year, chosen for their demonstrated impact on real lending operations. Smart Capital Center earned an invitation to the 2026 session, where it presented its end-to-end AI platform to an audience of industry executives actively shaping the future of CRE finance.

It refers to technologies that analyze large volumes of property, borrower, and financial data to support underwriting, risk monitoring, and portfolio management. AI systems can extract information from documents such as rent rolls, financial statements, loan agreements, and appraisal reports, allowing lenders to analyze deals more efficiently and identify potential risks earlier.

AI tools can extract financial and property data from borrower documents, populate underwriting models, and highlight potential risk indicators. This allows underwriting teams to focus more time on credit analysis and investment judgment rather than manual data entry and document review. The most advanced implementations also benchmark extracted assumptions against market data in real time, surfacing discrepancies before a credit memo reaches committee.

AI can analyze a wide range of documents used throughout the loan life cycle, including rent rolls, operating statements, borrower budgets appraisal reports, offering memorandums, inspection reports, loan agreements, insurance certificates, and asset management reports. By extracting structured data from these materials, lenders can create a more connected and searchable knowledge base across their portfolios — replacing static document archives with an active intelligence layer.

AI compares information across multiple documents and data sources simultaneously to identify inconsistencies or unusual patterns. For example, AI can analyze differences between rent rolls and financial statements, compare underwriting assumptions with appraisal projections, or evaluate borrower-reported performance against market data. These cross-document signals can help analysts identify potential fraud risks earlier and more systematically than manual review allows, particularly as generative AI has made plausible-looking fraudulent documents easier to produce.

A connected intelligence layer is a centralized system that aggregates information from multiple operational workflows across the loan life cycle. Instead of storing documents and data in isolated systems, institutions capture structured information that flows between underwriting, servicing, asset management, and portfolio monitoring functions. This creates a more unified view of loan performance and risk — and enables institutional knowledge preservation when team members transition roles or leave the organization.