AI in Commercial Real Estate

June 30, 2026

AI in Commercial Real Estate

June 30, 2026

According to the FBI’s 2024 Financial Crimes Report, real estate fraud schemes, including title fraud, identity-based ownership transfers, and occupancy misrepresentation, remain among the fastest-growing categories of financial crime in the United States, with CRE transactions increasingly targeted due to deal complexity and the multi-party entity structures that obscure true beneficial ownership. For lenders and investors, the cost of inadequate commercial real estate ownership verification surfaces at closing as a title defect, post-funding as a fraud loss, or during regulatory examination as a due diligence gap.

This analysis draws on Smart Capital Center, a CRE AI platform processing 1B+ real-time signals across 120M+ properties, used by institutional lenders, investors, and asset managers including JLL and KeyBank, to compare traditional and AI-powered approaches to commercial property ownership verification across each stage of the due diligence workflow.

The scale of the problem at the transaction level is well-documented by the industry’s own data. According to a May 2024 survey of 783 title insurance companies conducted by the American Land Title Association (ALTA) and ndp | analytics, 28% of title insurance companies experienced at least one seller impersonation fraud attempt in 2023, and 19% reported an attempt in April 2024 alone – a pace that indicates these schemes are no longer isolated incidents but a routine operational risk for anyone processing CRE ownership transfers. ALTA CEO Chris Morton has stated publicly: “Fraud is not a side issue in housing; it is part of the affordability story. The FBI’s latest data shows real estate fraud is growing in a threat environment shaped by impersonation, business email compromise, and AI-enabled deception.”

The verify ownership of property process in CRE is deceptively complicated. A single asset may be titled in an LLC owned by a holding company registered in a different state, controlled by a trust, with beneficial interests distributed across multiple individuals – none of whose names appear on the deed. Traditional due diligence that stops at the title search is looking at the surface of a structure that may extend several layers deeper.

The real estate fraud risk compounds here. Sophisticated schemes rarely rely on a single forged document. They work through a pattern of consistent but false records. Ownership transferred through a series of related entities, stated occupancy that does not match listing data, tax records with delinquencies that predate the current ownership claim. A reviewer checking any one record in isolation will see nothing unusual.

Manual verification reviews documents one at a time. It rarely catches patterns that only appear across multiple documents. For more on how real-time CRE data sources close this gap, the structural case for live data over static records applies directly to ownership verification.

Standard commercial real estate ownership data workflows involve four manual research steps, each with its own depth limitation:

• Title search: Examines the chain of recorded deed transfers from current ownership back through prior holders. Identifies encumbrances, liens, and easements but does not surface beneficial ownership behind entity holders or cross-jurisdiction structures.

• County assessor and recorder records: Provides the legal owner of record and tax payment history at the county level. Coverage is inconsistent across jurisdictions, update frequency varies, and no cross-state aggregation is available through public portals.

• Secretary of State entity filings: Confirms legal existence, registered agents, and officer or member information for LLCs and corporations. Does not reveal beneficial ownership beyond what the entity voluntarily disclosed at formation, and does not surface nominee structures.

• Manual entity structure mapping: An analyst traces the ownership chain by pulling Secretary of State records across multiple states, identifying each nested entity, and attempting to map ultimate beneficial ownership. This process can take days on complex structures and is highly dependent on the quality of public records in each jurisdiction.

AI-powered commercial real estate ownership data platforms aggregate county deed records, Secretary of State filings across all 50 states, UCC filings, and tax records into a single interface, then apply entity resolution logic to map the ownership chain automatically. Where a manual reviewer would need to pull records from three states and cross-reference four entity names, the AI produces a consolidated ownership graph in minutes.

Smart Capital Center surfaces commercial property ownership information from authoritative, county-level sources, with every data point linked to a clickable source citation. A lender reviewing an entity structure sees the specific record that supports it, reviewable on demand.

One of the most consistent fraud patterns in CRE lending involves stated occupancy that does not reflect actual conditions. A borrower submitting a rent roll showing 92% occupancy on a retail property that has three active vacancy listings on commercial listing platforms is presenting two irreconcilable data sets. Manual due diligence rarely catches this because the listing check is a separate, optional step that most workflows do not mandate.

Smart Capital Center cross-checks stated occupancy against live listing data and other market signals automatically, flagging discrepancies before they reach the credit committee. For a detailed look at how AI fraud alerts work across the CRE finance workflow, see Smart Capital Center Launches AI Fraud Alerts for CRE Finance.

Fraud in CRE is rarely one document. It is a pattern of consistent anomalies across documents and time periods. AI identifies these patterns by analyzing signals that no manual reviewer would connect in the course of a standard due diligence workflow:

• Rapid, multi-step ownership transfers through related entities in the 12 months preceding a refinancing or sale

• Tax delinquency records that predate the current ownership claim and were never disclosed

• Negative news or litigation records associated with principals that do not appear in standard lender databases

• Inconsistencies between the legal description in the deed and the property details in the OM or appraisal

None of these signals is individually conclusive. That is exactly why human reviewers miss them – each looks individually unremarkable. AI flags the pattern across all of them simultaneously, with every alert backed by a clickable source so the analyst can investigate rather than rely on the system’s conclusion alone.

Verification must replace trust. A one-time ownership check at origination catches what is true on the day the loan is funded. It does not catch a fraudulent transfer six months later, a tax delinquency that accumulates post-closing, or a change in beneficial ownership that triggers a due-on-sale clause.

The structural answer is continuous monitoring rather than periodic spot-checks. Smart Capital Center logs every verification action and makes the full review record exportable for compliance purposes, so the audit trail exists whether or not a human remembered to document each step. When something material surfaces, the notification reaches the asset manager with a source citation attached.

According to FinCEN’s 2024 Beneficial Ownership Reporting guidance, financial institutions are under increasing regulatory pressure to document the ongoing monitoring process. A verification trail that is logged, sourced, and exportable satisfies this requirement.

The cost of passive verification is measurable. According to the ACFE’s Occupational Fraud 2024: A Report to the Nations, fraud schemes detected through passive methods persisted an average of 24 months before detection, compared to 6 months for schemes caught through active automated monitoring. In a CRE lending context, that 18-month gap is the interval during which a fraudulent ownership transfer, an undisclosed beneficial owner change, or an accumulated tax delinquency remains invisible in the lender’s portfolio. Continuous, automated verification closes that window.

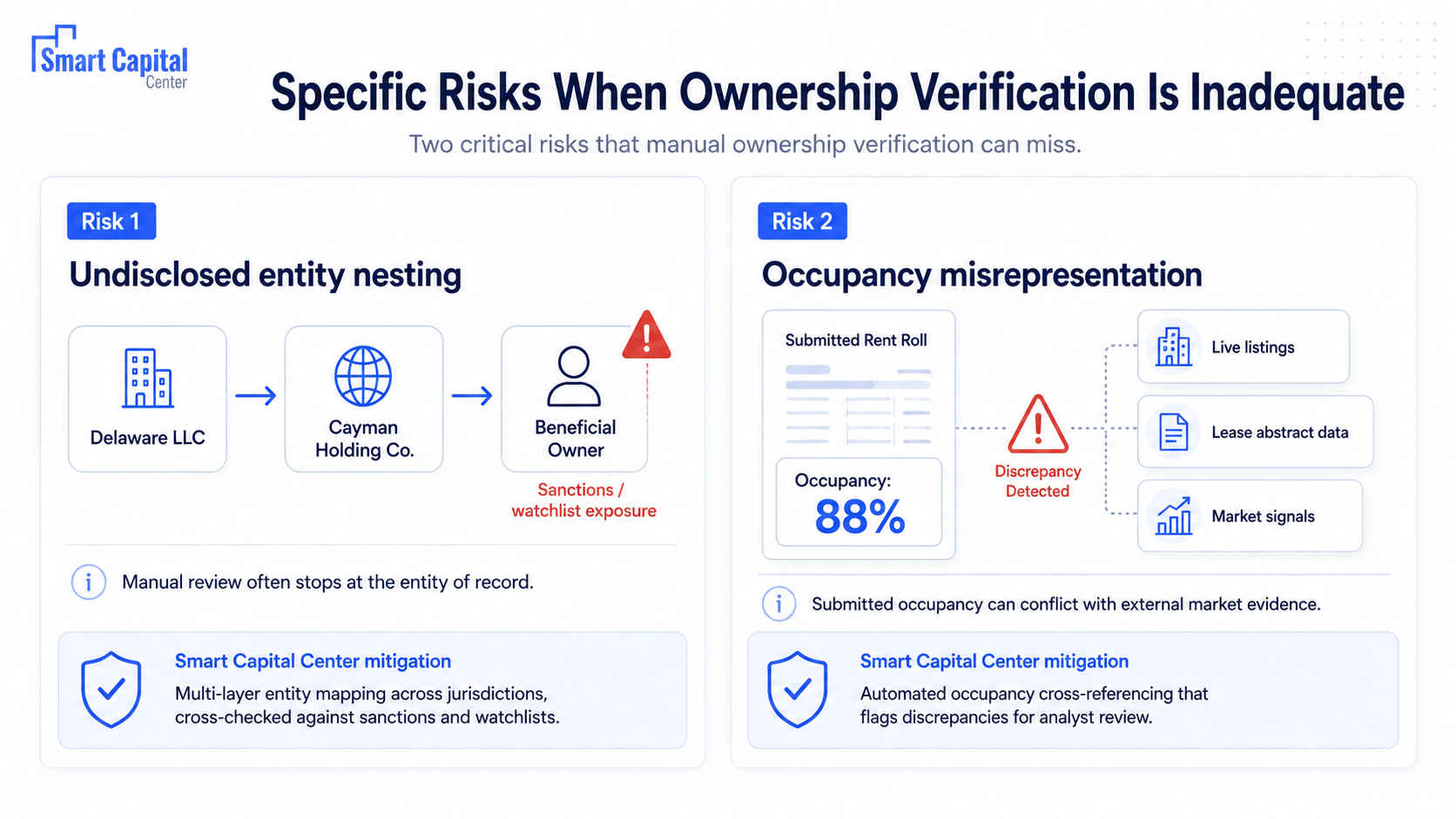

A loan originated to a Delaware LLC whose sole member is a Cayman-registered holding company, whose beneficial owner appears on an OFAC sanctions list, can pass a standard title search and Secretary of State check without surfacing the compliance exposure. The manual workflow checks the entity of record. It does not follow the chain to the ultimate beneficial owner.

Smart Capital Center mitigates this through multi-layer entity mapping that traces ownership chains across jurisdictions automatically, surfacing beneficial owner information and cross-referencing against sanctions and watchlist databases, with every finding linked to a verifiable source record.

A rent roll showing 88% occupancy that is inconsistent with current vacancy listings, lease expiration data from the property’s own lease abstracts, or foot traffic signals for the subject address represents a fraud risk that no amount of rent roll scrutiny will catch, because the fraud is in the rent roll itself. The cross-check requires an external data source.

Smart Capital Center mitigates this through automated occupancy cross-referencing that compares stated figures against live listing data and market signals, flagging discrepancies for analyst review before the credit package advances.

The lenders and investors who underwrite fraud risk the least are those who have made verification continuous, pattern-aware across every stage of the deal and ownership lifecycle.

Smart Capital Center makes commercial real estate ownership verification structural rather than optional, surfacing property history, entity structures, occupancy signals, tax records, and negative news in a single interface, with every alert backed by a clickable source and every review action logged for compliance.

Build a verification trail that holds up in credit review, regulatory examination, and post-close audit. Book a demo with Smart Capital Center.

A title search confirms the recorded deed holder but does not surface beneficial ownership behind entity structures, nested LLCs, or cross-jurisdiction holding companies. Effective verification requires pulling Secretary of State records across every state in which ownership entities are registered, cross-referencing against sanctions databases, and tracing the ownership chain to the ultimate beneficial owner. AI-powered platforms automate this multi-layer mapping, completing in minutes what manual research takes days to produce.

County assessor and recorder records provide deed history, legal owner of record, tax payment status, and property characteristics. Secretary of State filings provide entity registration, registered agent, and officer or member information for the entity of record. Neither source reveals beneficial ownership beyond what was disclosed at entity formation, and neither aggregates cross-jurisdiction information automatically. Smart Capital Center consolidates these sources into a single interface sourced from authoritative, county-level records, with clickable citations for every data point surfaced.

Manual due diligence reviews documents sequentially. AI analyzes patterns across documents and time periods simultaneously, identifying rapid ownership transfers through related entities, tax delinquencies predating the current ownership claim, occupancy figures inconsistent with live listing data, and negative news associated with beneficial owners. No single signal is conclusive. The fraud pattern is in their combination, and that combination is invisible to a reviewer checking each record in isolation.

AI cross-references the stated occupancy on a borrower-submitted rent roll against live listing data, market vacancy signals, and lease abstraction data from the property’s own documents. When stated occupancy and market-sourced occupancy diverge materially, the platform flags the discrepancy for analyst review with the source data attached. This cross-check catches the most common form of occupancy misrepresentation, where the fraud is in the submitted document itself.

Regulators and bank examiners reviewing CRE due diligence expect documentation of the process used to reach it: which records were checked, when they were reviewed, what the reviewer concluded, and how discrepancies were resolved. Smart Capital Center logs every verification action automatically and makes the full review record exportable, satisfying FinCEN beneficial ownership reporting requirements and OCC/FDIC examination standards.